| What the Plunging Aussie Dollar Means for You |

Monday, 17 October 2022 — Melbourne, Australia  | | By Greg Canavan | | Editor, The Daily Reckoning Australia |

|

[7 min read] In today’s Daily Reckoning Australia, see what we are telling our paying subscribers. The Aussie dollar — an indicator of global economic growth — is struggling…a sign that something is wrong. What are the impacts? How does this affect your wealth? Read on to find out… |

|

Editor’s note: Last week, our Editorial Director Greg Canavan wrote to our paid subscribers in The Insider after a plunge in the Aussie dollar’s value. There is a myriad of effects that this creates for the Aussie economy, and it’s important that Aussie investors are aware of them — which is why we want to share this insight with you today. There are downsides to a lagging Aussie dollar, no doubt, but there are also benefits. If we plan accordingly, there’s a way to prepare our investments to be primed to rise when the bull market returns. Enjoy…

Dear Reader, As I write this on Wednesday morning, the Aussie dollar is trading at around 62.8 US cents. It’s the lowest it’s traded since April 2020, during the COVID panic. Before that, you have to go back to the dark days of the GFC in November 2008. And before that to the early 2000s, with the rise of China and globalisation. You can see this in the long-term chart below:

The Aussie dollar is a great barometer of global economic growth. When it’s as weak as it is now, that tells you something is wrong in global commerce. That ‘something wrong’ is rising interest rates worldwide. As evidenced by the sharp fall in the Aussie dollar over the past few weeks, those rate rises are now starting to bite. As I mentioned in Monday’s Insider, monetary policy acts with a lag. And we don’t know how long that lag is. In his 1969 book The Optimum Quantity of Money, Milton Friedman said that monetary policy acts with ‘long and variable lags’. He, therefore, argued for rule-based rather than discretionary monetary policy. Given the hole that central bankers have dug for us over the past few decades, it’s hard to argue that Friedman had it wrong. Anyway, the point is the same one I’ve been making for a while now: The Fed continues to tighten while looking for evidence of its effect in lagging indicators. The sharp decline in the Aussie dollar is just another example of the rapid slowdown in global growth occurring right under the Fed’s nose. But it’s more than just that. Flexible exchange rates mean currencies act as shock absorbers. What made the Great Depression so bad in the 1930s (aside from easy money in the lead up) was the rigidity of the currency system at the time. Most major currencies were on a type of gold standard. So in the Great Depression, labour took a hit, as well as capital. The US dollar stood strong. It was only in April 1933 that Roosevelt devalued the dollar against gold, nearly four years after the Depression began. By that time, unemployment was around 25%, the banking system had collapsed, and the Dow Jones Index had already plunged 80% from top to bottom. These days, currencies move relative to other currencies, so as not to inflict such harsh outcomes on labour and capital. Everyone is impacted in some way by currency movements. Some benefit, some lose. But the idea is that pain is spread in a broad manner rather than narrowly. For example, a weaker Aussie dollar means imported goods cost more. It’s the market’s way of trying to discourage consumption and encourage production. But this can also feed into the inflation pressures Australia is already dealing with, putting pressure on the RBA to raise rates further. On the other hand, the weaker dollar makes our exports cheaper in the eyes of foreign buyers. This is good for our food producers and other commodity exporters. But if they need to invest in imported plants and equipment to build new mines and/or production capacity, it increases the cost of this initial investment. Another area that will likely benefit from a weaker Aussie dollar is high-end real estate. If you’re a cashed-up US investor and see that the Aussie dollar is down nearly 20% against the greenback in six months, a falling real estate market here all of a sudden looks very attractive. You can see the other impact of currency movements in the stock market. With the Fed raising rates and the US dollar the world’s reserve currency, the greenback is the only game in town. It’s by far the strongest-performing currency this year. That’s part of the reason why US markets are down heavily this year while the Aussie market has done much better. For example, the S&P 500 is down around 25% from its peak. Meanwhile, the ASX 200 is only down around 12.5% from its peak. However, if I denominate the ASX 200 in US dollars, as you can see below, it’s down more than 27% from its high:

So adjusting for currency movements, the Aussie market is on par with the US. Can you see now how floating rate currencies can cushion the effects of global capital flows and economic currents? But it can only absorb so much before other factors come into play — like imported inflation forcing the RBA to raise rates even further. There are many examples in history (especially in developing markets) where central banks have to raise rates to defend their currency. If history is any guide, it’s probably getting close to a bottom for the Aussie dollar here. But in the short term, with the Fed pushing the US into recession, you can’t rule out more downside. Advertisement: What to Do in a Bear Market Should you sell everything and allow inflation to erode your cash? Or hold on and hope for the best? Well, market analyst Greg Canavan offers a third option — a bear market survival plan. Access it here. |

|

Much will depend on this week’s (lagging) inflation figures, due out on Thursday in the US. A better-than-expected number for September should see markets — and the Aussie dollar — rally sharply. But if it remains higher than forecast, all hell could break loose. There’s one other currency impact I want to point out. It relates to commodities and what our producers receive for their goods. You see, when the Aussie dollar falls, and the US dollar price of a commodity remains stable, the Aussie dollar price rises. That’s been happening lately, especially with gold and oil. In the last few weeks, the Aussie dollar gold price has jumped by around $150/ounce to $2,650. Brent crude, priced in Aussie dollars, has gone from $130/bbl to $150/bbl. Not all companies benefit uniformly from this rise. Some have US dollar contracts, and in the case of the big energy companies, they report in US dollars anyway. But overall, the rise in price is beneficial to Aussie-based producers. In the case of gold, the miners’ share prices just aren’t responding. I’ve shown the chart below before. The gap between the Aussie-dollar gold price and the ASX Gold Index just keeps getting wider:

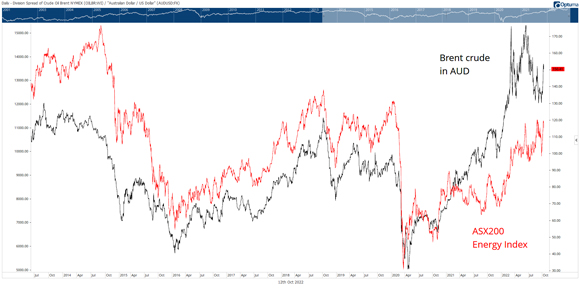

That just shows you how deep a bear market gold stocks are in right now. But when the turn comes, the gains will be substantial, in my view. The ‘discount’ on energy stocks isn’t as great. The chart below shows Brent crude in Aussie dollars versus the ASX 200 Energy Index. Energy stocks have been in a bull market, unlike gold stocks:

But there’s still a discount there. It’s like the energy stocks aren’t convinced that high oil prices will remain. Maybe with the Fed on an inflation war path, oil prices will succumb to demand destruction in the short term. As I’ve pointed out before, even with the dollar so strong and Biden depleting the Strategic Petroleum Reserve to its lowest levels since the early 1980s, oil prices remain strong. And thanks to the weak Aussie dollar, prices in the local currency aren’t far off the all-time highs reached just a few months ago. That’s why you’re still getting smashed at the petrol bower. This brings me back to inflation. A reader recently asked how I can be both bullish on oil and think inflation is heading lower. I’ve run out of time and space today, but I’ll answer that question in an upcoming essay.

Regards,

Greg Canavan,

Editor, The Daily Reckoning Australia

PS: To see that upcoming essay, you’ll need to become one of our paying subscribers. If you’re interested in Greg Canavan’s insights, you can sign up for his service, Fat Tail Investment Advisory, here.

| | By Bill Bonner | | Editor, The Daily Reckoning Australia |

|

Dear Reader, A lot of red on the screen last Thursday. The latest inflation readings were worse than expected. The Dow dropped 500 points. Remember, we’re only in the very first stage of what we believe will be a multistage disaster, like a traffic pile-up on I-95 during a foggy morning rush hour. After the Bubble Epoch, created by misters Greenspan, Bernanke, (Ms) Yellen, and Powell, came consumer price inflation. It is still with us. From Bloomberg: ‘US Core Inflation Seen Returning to 40-Year High as Rents Rise’: ‘CPI excluding food, energy probably rose 6.5% from year ago ‘Report expected to keep Fed on path to big November rate hike ‘A key US inflation measure due Thursday is set to return to a four-decade high, underscoring broad and elevated price pressures that are pushing the Federal Reserve toward yet another large interest-rate hike next month.’ And here’s CNBC with the latest on wholesale prices: ‘Wholesale prices rose more than expected in September despite Federal Reserve efforts to control inflation, according to a report Wednesday from the Bureau of Labor Statistics. ‘The producer price index, a measure of prices that U.S. businesses get for the goods and services they produce, increased 0.4% for the month, compared to the Dow Jones estimate for a 0.2% gain. On a 12-month basis, PPI rose 8.5%, which was a slight deceleration from the 8.7% in August.’ The next shoe The inflation numbers guarantee that we will stay in this deflation stage of the disaster at least a bit longer. Then, something will give. It could be a major pension fund, such as CalPERS, with half a trillion in assets. It could be a Wall Street finance house, such as BlackRock, with US$8.5 trillion in assets. Or it could be a big corporation forced into bankruptcy by rising interest payments. The longer the Fed remains on course — to exterminate inflation — the closer we get to the ‘pivot’, when a financial shock keeps it from getting the job done. The big questions are: When will the Fed do its pirouette? And what happens then? Most people think the Fed will soon go back to normal — which, for them, means rising stock prices, with inflation subdued. Maybe it’s just our imagination. But we notice a big difference between how young people look at the situation and how older people do. Anyone younger than 60 has no adult recollection of any financial world other than the one we’ve had since 1980. They thought that was normal. And after this hissy fit is over, and the Fed turns around, they believe things will go back to the ‘normal’ they have known. But there was nothing normal about the 1980–2020 period. Is it normal for stock prices to multiply 36 times — as the Dow did between 1982 and 2021? Is it normal for real bond yields to drop from the high teens down to less than zero? Is it normal for the Fed to ‘print’ more new money in 18 months than it had in nearly 100 years…or for the federal government to multiply its debt by 30 times…even as its carrying cost (interest payments) went down?

Back to the future We could go on. There were more freaks in this show than in Barnum & Bailey’s circus — zombie corporations, goofy cryptos, billion-dollar valuations for companies with no plausible way to earn money. And yet…for so many callow investors…that was planet Earth — the way things have been…the way they are…and the way they shall ever be. They think stocks always go up ‘over the long run’. Yes, there may be sell-offs, they admit, but a balanced portfolio of stocks and bonds will always pay off. Maybe. But not necessarily in your lifetime. You’ve got to go back before the ‘80s…and you’ve got to look at it in terms of real money — gold — to see what ‘normal’ really looks like. If you’d bought stocks in the late 1920s, you would have gotten all 30 Dow stocks in exchange for 16 ounces of gold. Then by 1933, you would’ve lost 90% of your money…and waited another 26 years to break even again. Yes…prices move in cycles…but they are long cycles. Same thing in the 1960s. Inflation was dogging the economy then, as it is now. And then, a stockbroker would have told you what he will tell you now — ‘don’t worry about market timing; just get good companies and hold on’. If you’d owned stocks in the mid-‘60s, your 30 Dow stocks would have been worth as much as 24 ounces of gold. Then, it took 15 years for the market to hit a bottom, in 1980…and you’d be down 93%. Then what? You would have waited another 17 years to breakeven. Altogether, if you’d bought stocks at age 40 in 1965, you’d be 72 years old in 1997…with not a penny of capital gain to show for it. But imagine that you followed your broker’s advice…and you just stuck with the program. Today, you’d be 97 years old. And instead of stocks worth 24 ounces of gold, as they were in 1965, they would be worth 17 ounces! Congratulations, your stocks lost 30% of their value over the last 57 years. (Not including dividends.) Is there a better way? Maybe. Tune in tomorrow...

Regards,

Bill Bonner,

For The Daily Reckoning Australia

Advertisement: ‘Hidden’ EV Stocks for Less than $1 The EV boom and lithium shortage is a ripe opportunity for investors. And small-cap expert Callum Newman has found three ASX stocks that can help you capitalise. The market doesn’t know about them yet, which is why you can pick them up for less than $1. Click here to learn more. |

|

|