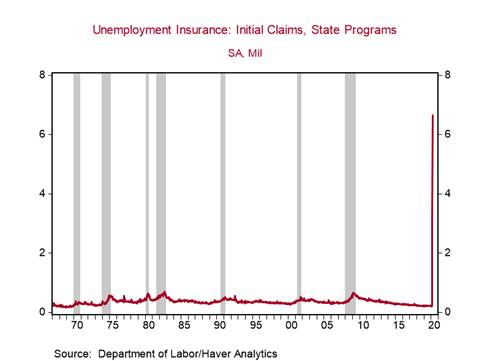

*U.S. initial jobless claims continued to set new highs during the week ending March 28, doubling to 6.6m from 3.3m in the prior week, bringing the two-week total to 9.9m, which is almost twice the 5.8m persons counted as unemployed in February, when the unemployment rate was 3.5% (Chart 1).

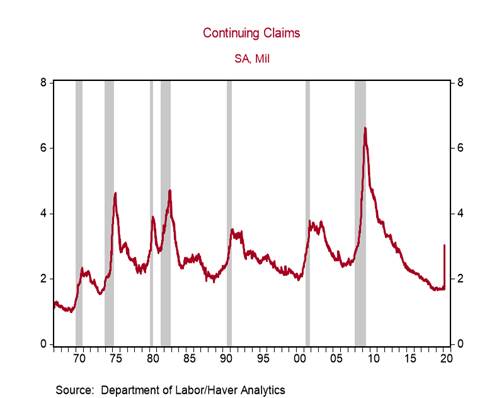

*Continuing claims for unemployment insurance, which are reported with a two-week lag, increased to 3.0m during the week ending March 21 from 1.8m (Chart 2). During the Great Recession of 2008-2009, it took 1.5 years for continuing claims to increase by 3.9m to 6.6m; this time it has happened over the span of a few weeks.

States reporting the largest number of initial jobless claims (in non-seasonally adjusted terms) were California (879k), Pennsylvania (406k), New York (366k), and Michigan (311k). With more states issuing stay-at-home orders this week, initial jobless claims could continue to set new highs during the first half of April.

ADP/Moody’s Analytics yesterday reported that U.S. private payrolls declined by 27k in March, but it mimics the Bureau of Labor Statistics’ (BLS) Official Employment Report (set for release tomorrow) in measuring payrolls during the pay period that includes the 12th of the month. Therefore, both the ADP and BLS numbers released this week are stale and do not reflect the millions of jobs that are currently being lost as reflected in the weekly jobless claims data. We expect the BLS to report that nonfarm payrolls declined by 100k in March and forecast that its April Employment Report (scheduled for release on May 8) will reflect millions of job losses that pushes the unemployment rate above 12%.

The Coronavirus Aid, Relief, and Economic Security (CARES) Act that was signed into law last week boosts unemployment insurance by $600 per week for four months and expands eligibility to include “GIG employees” who are estimated to total around 20 million. These expanded benefits are a good initiative that will entice more persons to file jobless claims to mitigate financial losses, keeping the initial jobless claims count elevated for some time.

The Paycheck Protection Program provision in the CARES Act forgives the amount of principal from eligible Small Business Administration (SBA) loans equal to the sum of expenses for payroll, and existing interest payments on mortgages, rent payments, leases, and utility service agreements if small businesses retain employees. If this provision works effectively it would reduce job losses and also allow the economy to reopen more quickly once the acute stage of this pandemic is over.

Chart 1:

Chart 2:

Roiana Reid, [email protected]