A Message from Golden Portfolio U.S. Treasury Secretary Scott Bessent is the man who oversees America’s $37 trillion debt load. No one has more insight into what’s happening with the US dollar… mounting US debt… of the likely changes coming to the US monetary system. Not surprisingly… His largest personal investment holding is gold. Not tech stocks… Not U.S. Treasuries… Not “safe-haven” index funds or ETFs… Gold. When the U.S. Treasury Secretary’s largest personal holding is gold… That’s known as “a clue.” Wanna know who else sees what Bessent does? Warren Buffett. At last count, Buffett is sitting on $330 billion in cash. But he knows he cannot hold this much cash forever. - Cash is losing purchasing power at roughly 22% a year (measured in gold).

- The US political system is printing money like it’s Monopoly cash

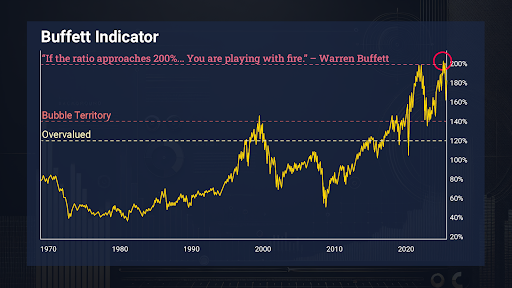

- And – most importantly – Buffett’s favorite indicator currently sitting just over 200% – which means US stocks are still more overvalued than they’ve ever been.

Every time the “Buffett Indicator” reaches a peak… Gold goes on a tear for a decade or more. Every. Single. Time. That’s why I believe Buffett is preparing to buy the one gold miner large enough to protect his cash. And here’s the kicker… This large-cap miner is still trading at a 40% discount to its free cash flow. What’s more, Trump recently tapped the CEO of this mining powerhouse to help lead America’s mining revival! Add it all up and here’s what you get: - The US Treasury Secretary is positioned for a major move in gold… and move that’s sure to come when he authorizes all the money required to finance more deficit spending.

- The world’s greatest investor needs a major gold position to protect his $330 billion cash pile… and there’s only one company big enough to do it.

- Trump has entrusted the CEO of the #1 major gold miner to lead a Renaissance in US mining.

Final confirmation of my prediction could come by August 15th — when Buffett’s 13F filing hits the tape. You want to be in position before that happens. You still have time to “front run” the world’s greatest investor by taking a stake in the one mining company big enough to handle his $330 billion cash hoard. That’s why I’ve prepared a private gold briefing with: - The name and ticker of the company Buffett is likely targeting

- Four tiny gold miners with “anomaly” upside potential up to 100X

- A special bonus pick that doesn’t mine gold at all – collects royalty income on mines it financed

Go here to get the name and ticker of Buffett’s next big move into gold. Regards, Garrett Goggin, CFA, CMT

Chief Analyst and Founder, Golden Portfolio

Today's Bonus Article Power Solutions International Poised for 75% UpsideWritten by Thomas Hughes

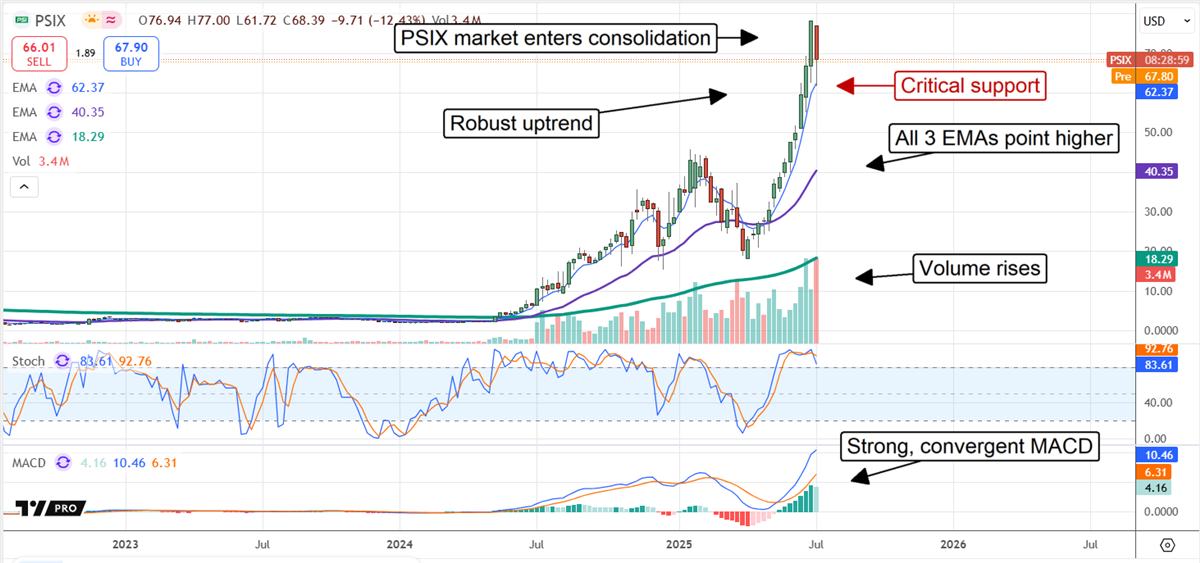

If you have wondered whether Power Solutions International’s (NASDAQ: PSIX) stock rally is played out or has room to run, the charts say this market is strengthening and has room to run. A lot of room to run. The company's weekly chart is a textbook example of a bull market gaining strength. It shows the potential to rise by another 75% before reaching a significant top. Bullish signals include the price action, which is trending strongly higher, the MACD, which is robust and converging with the highs, and volume, which is also strong, rising, and converging with the highs. Together, they amount to a strong technical signal; the only problem is that the price is pulling back in mid-July.

However, some interesting possibilities emerge, assuming the market is entering a consolidation, potentially forming a triangle or flag pattern. The market will create a continuation pattern in that scenario and bring the full magnitude of its move into view. A bullish flag pattern is typically the middle or within the mid-range of a larger movement, which, in this case, could extend by an amount equal to the rally that preceded it. That’s a solid $60 movement, potentially putting this market at $140 by the end of this year. Power Solutions International Is an AI Play With Legs Power Solutions International is an outside-the-box AI play whose business is essential to the industry: power and power management. Its custom engines and power solutions are used for critical backup power supply, seamlessly integrated into the data center infrastructure. That is a vital element in an industry reliant on steady, reliable power, and PSIX doesn’t stop there. Power Solutions International also provides power management equipment and services, essential for the power-consuming data center industry. Other business drivers include its impact on end-user compliance requirements, such as environmental. PSIX solutions can be used with multiple fuel types, including natural gas, propane, and biofuel. It is also a diversified business model with operations spanning industrial, transportation, and power system markets. The critical takeaway is that Power Solutions International’s revenue growth accelerated under the influence of AI. The Q1 results revealed a 42.3% year-over-year (YOY) increase, which outperformed MarketBeat’s consensus by 2500 basis points and led management to provide strong guidance. The consensus is for revenue growth to continue sequentially, sustaining a high-double-digit YOY pace through the end of the year, and is likely too cautious. The consensus is expected to be low due to the low number of analysts covering the stock and the amount of revision activity in 2025. The analysts and institutional activity is tepid in 2025 but offers potential for increased activity. MarketBeat tracks a single analyst and reports less than 25% institutional ownership. The single analyst rates the stock as a Buy, with more Buy ratings expected. Institutions have been buying on balance in 2025, a trend likely to strengthen over the coming quarters. Power Solutions International Makes Profits Today Unlike many small-cap tech stocks, this one makes money today. The company’s margins are not only positive in 2025 but are also widening under the influence of revenue leverage, operational improvement, and spending controls. Gross margin widened by 270 basis points in Q1, while SG&A grew much slower than revenue, resulting in net income increasing by nearly 170% and adjusted EPS just over eight cents, 37 cents higher than expected. Cash flow is also positive, allowing PSIX to reduce debt in Q1. The company’s cash position is also solid, leaving equity up roughly 30% and the business in a flexible financial position. Management aims to leverage the balance sheet, using debt to fund growth and drive value gains for shareholders. |