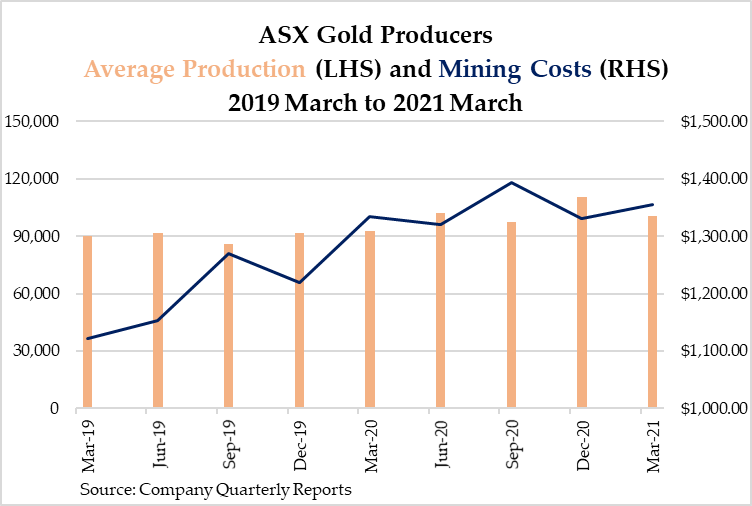

Industry consolidation The larger industry players have seen a clear decline in their mines’ ore grades, leading to lower production. They have two choices — explore or buy new deposits or mines to grow. The latter is a faster but more expensive option. Several company boards opted for the latter. You saw several major acquisitions and mergers in the past year. This includes the Northern Star Mines Ltd [ASX:NST] and Saracen Mineral Holdings Ltd [ASX:SAR] merge, to form the third-largest gold producer on the ASX in 2020. Also, Alacer Gold Corp [ASX:AQG] merging with SSR Mining Inc [ASX:SSR] in 2020, Regis Resources Ltd [ASX:RRL] purchasing a 30% stake of the Tropicana Mine from IGO Ltd [ASX:IGO] in April this year, and Evolution Mining Ltd [ASX:EVN] purchasing the Canadian developer Battle North Gold Corp [TSX:BNAU] in March this year. With this type of consolidation comes significant integration costs. There may be synergies in the longer term, but first comes some pain of cutting redundant staff, merging different companies’ administrations, and also the hidden costs of merging two company cultures. Then you also have the costs associated on the mine sites. Several company mergers and mine acquisitions involve bringing undeveloped mine deposits into production. The rising trend in the average production is partly due to companies buying existing mines and adding to their existing production. The industry consolidation in the last three years has been handled better this time by management than it was in the last gold rally from 2009–11. Adrian Day of Adrian Day Asset Management criticised management of gold companies in the past for spending like drunken sailors and hurting shareholders. He has recently been more forthcoming with praises instead. I agree with him. There are some purchases I have seen that are overpriced. But on the whole, these have been exceptions rather than the rule. The companies have better balance sheets this time too. Less debt and more cash in the bank to weather the storm. You are now beginning to see the fruits of some of these labours. What it means to you? The gold mining industry is going through some major changes as companies look to beef up their mine portfolios. Mining costs are rising. This could continue as the price of oil has doubled since late last year. However, the companies are generally in better shape than ever. Part of the reason gold stocks underperformed over the last year was that this type of consolidation period was going on as the gold companies jostled for assets and streamlined their costs as much as possible. The price of gold cooled too in the US. However, think of the long term. Gold companies can now sweat their assets at very good margins with Aussie dollar gold at around $2,350. My analysis says the upcoming three-month period is, historically at least, very bullish for gold stocks usually on the ASX. And that 20% decline over the last financial year? I call that a discount. I’m buying. Are you? God bless, Brian Chu,

Editor, The Daily Reckoning Australia PS: I’ve recently released a special report for this ‘golden’ three-month period. It contains my top five gold stocks to consider right now. Go here to get it. |