| The Real Estate Investment You Should Avoid at All Costs |

Thursday, 5 May 2022 — Albert Park  | | By Catherine Cashmore | | Editor, The Daily Reckoning Australia |

|

[5 min read] Dear Reader, I’ve banged on about the folly of investing in apartments for years. It’s often seen as a way into the property market at an entry-level price point. No one wants to take on too much debt in an environment where lending costs are going to continue rising. An established two-bedroom apartment in Melbourne, for example, transacts for anything from around $450–550K. It looks very affordable compared to detached housing. And with rental yields rising across all capitals, apartments are often spruiked as a good, ‘affordable’ hedge against inflation. But there are numerous unforeseen costs and headaches with investing in this sector. I’m not just talking about the fact that apartment prices have barely tracked the rate of inflation over the last 10–20 years. In recent weeks, I’ve been contacted by several owners wanting advice on selling apartments that have lost significant value since construction! I’m talking to the tune of $50–70K per unit. Furthermore, the apartments are situated in cities currently experiencing strong price growth: Brisbane and Perth. After hanging on for several years hoping the market would improve, they’re now resigned to selling at a loss. That’s not a nice situation to be in. Property prices always rise, don’t they? At least, that’s the story pumped by the real estate sector. Post-COVID, the situation has become worse. Home buyers want more space. There’s still an exodus of migration away from the major cities and, therefore, less demand for compact living. Then we have continued bad media regarding the quality of construction. Did you hear the recent news about Bond Square? It’s a large apartment complex in Spencer St, West Melbourne. Around 9–10 months ago, a six-storey car stacker collapsed. It crushed one vehicle and trapped about 30 others. Take a look: Luckily, no one was hurt. Although, rumour has it one owner had only just exited their vehicle in time. The thing is, the situation at Bond Square is now in limbo. No one is taking responsibility for the malfunction or repair. Residents are forking out thousands for hire cars and rideshares while still paying registration and monthly insurance on their trapped cars. Furthermore, the owners’ corporation has washed their hands of the situation! ‘According to the Owners’ Corporation, liability rested with Levanta Park, the Queensland company that supplied and installed the stacker. ‘The Owners’ Corporation warned it would “not be responding to any demands in respect of loss of access to your vehicle”. ‘Levanta’s lawyers fired back in a letter of their own and said: “Repairing and maintaining common property and associated fixtures and services is a function of the Owners' Corporation.”’

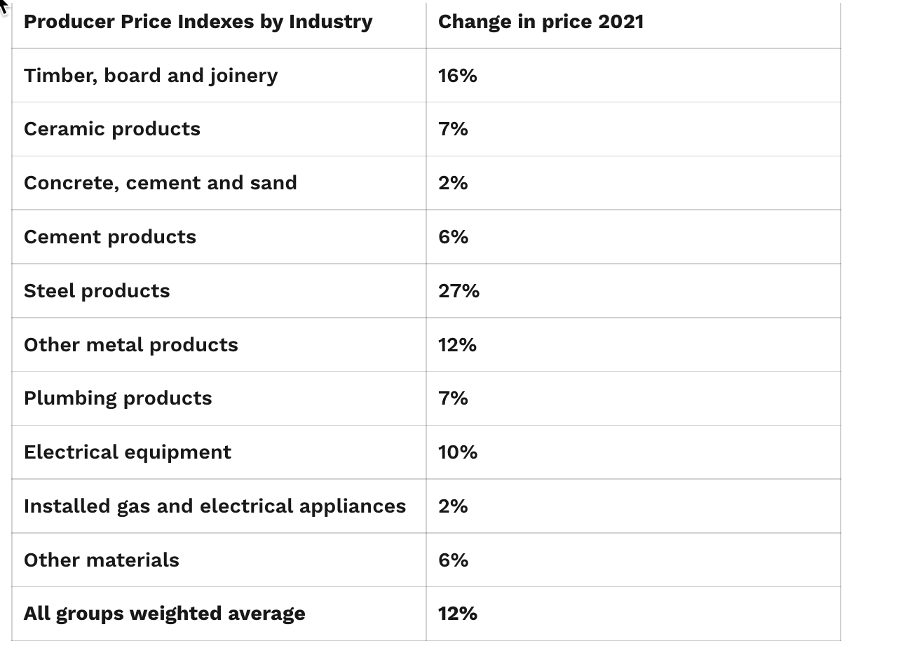

What a nightmare. These problems go to the core of the way strata management companies handle their finances. A colleague called me just this morning to discuss this — he’s trying to reform the sector. For example, some states have legislated sinking funds for apartment complexes. If you’re not aware, sinking funds collate payments that owners make each year, usually in line with 10-year management plans for the maintenance, repair, and replacement of items such as windows, lifts, roofs, and car stackers! However, oversight is lax, and the few payments collected usually end up sitting in term deposit accounts that can’t maintain pace with the rate of inflation. Especially not in today’s environment. If the payments are not made, the building loses value, and no diligent buyer will touch it. This becomes more significant when you consider the ongoing and escalating costs of construction. For example, in the December quarter of 2021, input prices for construction rose an average of 3.8%. Going forward, that’s an annualised 12%! Here’s a rundown: Advertisement: ‘A Mind-Boggling Opportunity for Growth’ That’s how one industry insider described this billion-dollar energy trend. Forbes says it may be ‘the keystone of the energy transition’. And one tiny Aussie stock is leading the charge. Find out which here. |

|

If apartment owners are with a management company that doesn’t plan for rising costs or — worse still — doesn’t take the time to invest the funds wisely, the consequences are dire. The owners are at risk of being left with a property investment they simply can’t sell. Don’t get me wrong, real estate can be a great hedge against inflation. Many owners have benefitted greatly over the last two years from rising rents and rocketing land prices. To put a figure on it, over the last 12 months alone, we’re talking a whopping $135.6 billion (or for investors, $40.6 billion) in land price inflation. Small rate hikes aren’t going to be enough to stall the market, as I explained the other week. But knowing what to invest in and where to invest is key. Equally so, when to get into the market and when to get out! You can find out more about that here. Best wishes, Catherine Cashmore,

Editor, The Daily Reckoning Australia  | | By Bill Bonner | | Editor, The Daily Reckoning Australia |

|

Dear Reader, Last week, we got news that the US economy is now in reverse. It’s no longer growing; it’s shrinking, backing up. Less income, fewer sales, fewer profits, smaller salaries — the whole shebang. Never, in our entire lifetimes, have so many lost so much so fast. MarketWatch has the shocking report: ‘The most concerning thing about Thursday’s report on U.S. gross domestic product for the first quarter wasn’t that the first line of the first table showed that real GDP fell at a 1.4% annual rate. It was the little-noticed news on line 34 showing that real disposable incomes fell for a fourth straight quarter. ‘Over the last four quarters, the purchasing power of after-tax household incomes plunged by $2.2 trillion (in 2021 dollars). That’s a 10.9% decline, by far the largest in the records dating back to 1947.’

Wait a minute. It’s worse than that. Real disposable personal income (as opposed to household incomes) for March was actually 20% below that of March 2021. No mystery. No magic. It’s just that old symmetry we’ve been talking about. Hopes flushed When COVID hit, the feds panicked. Donald Trump declared an emergency (there was none)…and started handing out money (there was none of that available either). And then, Joe Biden and his team continued the madness with another US$1.9 trillion in unnecessary spending of non-existent money. This tsunami of free money washed over a hunkered-down economy. Unable to spend the money, ‘savings rates’ rose like the plastic ball in a toilet tank. From an average of 6% the rate floated up to 34%. But then, of course, COVID receded, the masks came off, businesses opened up, and Americans flushed all that extra money into the economy. Prices rose, as you’d expect. The gimmies and stimmies soon petered out. And savings rates went right back down to 6%. GDP growth — which, in the last quarter of 2021, had been hoisted to 6.9% on the Fed’s US$3 trillion budget deficit petard — collapsed down to the aforementioned MINUS 1.4%. It was fun while it lasted. But now it’s over. And it causes us to wonder…what if? What if these things had not happened? What if the 21st century had never come…and things continued, more or less as, they had in the 20th century? What if the feds hadn’t squandered US$20 trillion (plus or minus) on wars and bailouts since 1999? What if they hadn’t shut down the economy in 2020…and spent money out the wazoo to make up for it? And what if the internet had never been invented? Sliding poors Access to the world wide web was supposed to bring unparalleled riches. After all, it was ‘information’ that separated the rich from the poor. The rich know how to make money. The poor do not. And finally, thanks to Microsoft and Google…that vital information was available to everyone. Even the humblest peasant in the dustiest, most windblown burg in the most dogsh*t country on Earth could fire up his laptop computer and discover how to do mergers and acquisitions! This knowledge was destined to blow out all the speed limits on the great highway of commerce and innovation, or so they said. And yet, since the Clinton years of the 1990s, GDP growth has dropped steadily…from nearly 4% down to this last quarter’s dismal reading of NEGATIVE 1.4%. So, what if the internet hadn’t come along? What if the growth rates of the 20th century continued? Pew Research reports: ‘Most of the increase in household income was achieved in the period from 1970 to 2000. In these three decades, the median income increased by 41%, to $70,800, at an annual average rate of 1.2%. From 2000 to 2018, the growth in household income slowed to an annual average rate of only 0.3%. If there had been no such slowdown and incomes had continued to increase in this century at the same rate as from 1970 to 2000, the current median U.S. household income would be about $87,000, considerably higher than its actual level of $74,600.’

There you have it. Or at least part of it. The ‘more to the story’ is that the feds gummed up the banking system with all their deadhead rules. And they fiddled interest rates into negative territory and brought forth an additional US$50 trillion — household, business, and federal — worth of debt so far this century. Meanwhile, the internet provided an around-the-clock circus, distracting the public from the real economy…and offering a cheap, hollow substitute for real knowledge. In 2001, the masses became experts on the geopolitics of the Middle East. In 2008, they mastered Keynesian economic theory. Then, in 2020, virology absorbed billions of hours that might otherwise have been put to productive uses. And now, they know all they need to know about the Russo-Ukrainian war…and Kim Kardashian! Without the internet, in other words, we might all be richer…happier… safer…and smarter… …but we wouldn’t have TikTok or NFTs, would we? Regards, Bill Bonner,

For The Daily Reckoning Australia Advertisement: This October Prediction Is Starting to Come True In October 2021, Vern Gowdie warned that four ‘code red’ investments could trigger a market crash. We’ve seen three out of the four so far... The downward spiral of tech stocks. $1 trillion losses in cryptos. A flattening bond yield curve. When will the final domino fall? And how can you prepare? Vern reveals the answers in this report. |

|

|