| The Post-COVID CBD Office Sector — a Good or Bad Investment? |

Thursday, 21 July 2022 — Albert Park  | | By Catherine Cashmore | | Editor, The Daily Reckoning Australia |

|

[5 min read] Dear Reader, Melbourne’s Comedy Theatre — constructed in 1928 — is set to undergo a major redevelopment. The $211 million plans include knocking down the rear of the theatre and expanding its stage to accommodate bigger acts — along with improving facilities to allow for disabled access. The project wouldn’t be feasible without funding via a joint venture between LaSalle Investment Management and theatre owners the Marriner Group. LaSalle have secured the air rights over the theatre to allow development of the office block at the rear that will cantilever over the theatre. The 23-storey office tower will spread across 222–240 Exhibition St. The communal spaces in the office building will be available for use by the theatre on weekends and evenings for rehearsals and entertainment. Here’s a mock-up of the proposed design:

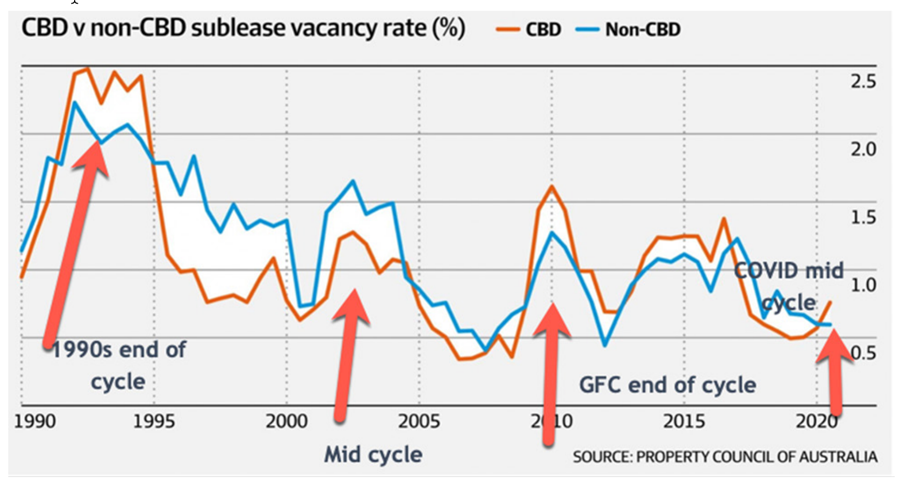

You might be wondering if there’s much demand for CBD office space. The sector was trashed through the pandemic — felt most severely in Melbourne — the lockdown capital of Australia. It was best monitored at the time via the sublease barrometre. To survive an extended downturn, office markets need to be generating rent and tenant demand. Subleasing is when firms unable to operate at full capacity put their offices onto the market to attempt to rent them out to someone else. The graph below is from the Property Council of Australia. It charts the trend of sublease vacancies over recent decades into the COVID panic. And not surprisingly, for those that understand the 18-year real estate cycle, it charts this also: In the early 1990s recession, the sublease vacancy rate peaked at around 2.5%.

Lesser surges were recorded during the mid-cycle real estate recession (the 2001 dotcom bubble), the 2008 Global Financial Crisis, and the most recent 2020/21 COVID-panic.

Since the lockdowns have ended, things have improved markedly.

Hybrid work arrangements have become increasingly common.

Sublease availability in Australia’s five largest cities decreased more than 100,000sqm in the year to June 2022.

The biggest changes were recorded in Melbourne, with an 81,300sqm decrease.

Still, things aren’t looking all that rosy elsewhere.

Geopolitical fractions, supply chain disruptions, rising cost pressures — as well as the Chief Medical Officer once again advising people to ‘work from home’ — has seen office vacancy rates increase in the second quarter of 2022.

Sydney’s vacancy rate nudged up to 13% and Melbourne 15% (according to data compiled by real estate advisory JLL).

Even Perth has a high CBD office vacancy rate — topping 20%.

Alongside this, incentives are at, or close to, peak levels.

Incentives are payments or rental concessions offered by a landlord of an office building to entice new or existing current tenants to sign onto a lease.

They can give the illusion that yields are healthy. But in reality, it’s a game of smoke and mirrors.

For investors, you could be buying a property that’s showing a 6% yield. But if the tenant has secured a 50% rental incentive the reality is half that. In an inflationary environment, it doesn’t look crash hot.

We’ll wait to see whether the proposed development above the Melbourne Comedy Theatre will be able to achieve full occupancy with or without incentives.

But for commercial investors — I’d be cautioning against investment of CBD office stock in favour of other commercial markets that are showing better returns.

Sincerely, Catherine Cashmore,

Editor, The Daily Reckoning Australia

Advertisement: Make these five money moves today for the chance to capitalise on the Biggest Boom In Aussie History It’s already sent stocks, property, and commodities through the roof. But two of our leading forecasters say there’s a total of $4 trillion still on the table. Here’s what smart investors can do to cash in. |

|

| | By Bill Bonner | | Editor, The Daily Reckoning Australia |

|

Dear Reader, ‘Forward the Light Brigade

‘Was there a man dismayed

‘Not tho’ the soldier knew

‘Some one had blunder’d’ The Charge of the Light Brigade, Alfred Lord Tennyson The headlines have been relentless. Ever since the beginning of the war of the Donetsk Oblast began, Russia has failed miserably. Its generals have been killed off. Its tanks have been sitting ducks. Its convoys have been stopped. Its targets missed. Its offenses halted. For the Russians, Ukraine has been the valley of death. Newsweek, yesterday: ‘Ukraine Destroys Two Military Ammo Depots, Hurting Russian Morale’. The Russian military was portrayed as ill-equipped, ill-trained, ill-disciplined, and hopelessly incompetent. Not once have we heard of a Russian victory…a Ukrainian killed, or a Russian who was not. At this stage, based on US news reports, it’s amazing that there is a Russian soldier left alive. But what if there were more to the story? We saw yesterday that Russia is where doomed empires go to die. 1709, 1812, 1941…Charles X11, Napoleon Bonaparte, Adolf Hitler — none fully recovered their Russian losses. So we wondered: will the US’s sanctions war, using its Ukrainian allies to do the dying, turn out any different? Drunk and sober We wonder not for geopolitical or ideological reasons. We have no Ukrainian flag on our walls. Nor a flag for the Russian Federation. Our only loyalty is to our own homeland…not someone else’s. Yes, ‘Maryland, My Maryland’ — land of esters and ‘bacca’…loudmouths and dimwits…Nancy Pelosi and Roger B Taney…drunk and sober. Even here, our sentimental attachments run no further north than the south bank of the South River. Beyond it…which is to say, from Annapolis to the Pennsylvania line…is foreign to us. As for Maryland south of the South River, it is a shame. Once so delightfully backward, quiet, and charming, it is now filled up with spill over from the greater Washington DC area…and thus culturally and economically dead. (One of the finest houses on the banks of the Chesapeake once the home of an honest contraband smuggler…is now owned by a disgraceful military contractor.) That is a digression…almost a non sequitur. But not quite. For now, we are expected to stretch our patriotism far beyond the Patapsco…and the Potomac…all the way to the banks of Dnieper. General de Caulaincourt begged Napoleon to stay out of Russia. Only a damned fool would want to fight there, especially in the wintertime, he said. Shouldn’t one of the US’s brass-bedecked heroes have warned Joe Biden too? Yes, maybe he should. But winter will come soon enough. The gods of war will have their say. Russia may not prove the pushover Biden had hoped. And ‘General Winter’ — the victor in both 1812 and 1944 — may not stop at the Ukrainian border. German experts are warning that their economy could contract by more than 12% if Russia shuts off its gas. Nearly six million jobs would be lost. Germans would shiver. Germans would fret and grow restless. And Germany, the great industrial powerhouse of the West — would have to capitulate. But we are just speculating… Quality versus quantity To back up a bit, the US war industry needs enemies. But it needs certain kinds of enemies — those that are unpopular in the US…and can do us little real harm. Little, largely defenceless nations are best. They are low-risk, high-reward targets. Lots of money to the industry; little chance of getting its butt kicked. In this respect, Russia is an outlier. It’s a nuclear power. But it had been rendered unpopular by endless charges of ‘interference’ in US elections. No serious evidence was ever presented, but it didn’t matter; the charge itself — though absurd — helped create the atmosphere the industry needed. Compared to the US, the Russian economy is tiny — roughly equivalent to Spain. But it’s not the size of the Russian economy that poses a challenge, it’s the quality of it. Over many years, the US economy has been pumped up by financialisation, fake money, and faddish technology. The Russian economy has not. Nobody buys the latest Russian fashions. Nobody buys fine Russian wines. And the only electronic entertainment produced in Russia with widespread appeal is pornography. Russia sells necessities — food, fertiliser, and fuel. Oh…and Russia is also a big producer of ‘industrial warfare’ ammunition, bullets, and artillery shells, for example. So, when we compare the two economies, what do we see? Russia — wheat, barley, seafood, nitrogen, phosphorus, potash, oil, gas, metals, and minerals…many of them essential to modern economies and standards of living. US — Facebook, Netflix, Google, Amazon, Microsoft, Twitter, Tesla, Walmart, Apple. A tale of two economies The US economy is much bigger. But how much is it fluffed up with things we mostly don’t really need? Entertainment. Distraction. Consumption. Do our most valuable US companies actually help us produce wealth? Or do they subtract it by wasting our most precious asset — our time? We don’t know. But we note that since the US became fully on-line — around about the beginning of this century — real GDP (goods and services) growth rates have declined; from 3% to 5% in the last half of the 20th century, they fell to 2%...down to…currently…less than zero! How much of the US economy is just foam, created by the Fed’s money printing and phony interest rates over the last 30 years? A week or so ago, we estimated the froth in household wealth at more than US$50 trillion. This is how much would vanish if the financialised economy were de-financialised…with stocks, bonds, and real estate marked down to more ‘normal’ levels. How would the two countries — Russia versus the US — stack up then? Maybe a better question is this: when push comes to shove, how important is the quality of output, compared to the quantity of it? If Facebook, oops...Metaverse, shut down, people would be disappointed. But would it really matter? They don’t make bullets in the Metaverse; they make them in Russia. And they don’t deliver gas from Netflix. It comes from Russia, too. And if it were turned off; what would be the effect? It looks like we’re going to find out. More to come…

Regards,

Bill Bonner,

For The Daily Reckoning Australia Advertisement: What you decide to do with your capital in the next few weeks… …will determine the success of your portfolio in the next few years Find out why here |

|

|