Editor’s note: Attention gold enthusiasts, investors, and speculators. Today is your last day to join ‘The 2022 Gold Investor Series’. We’ve gathered some of the biggest gold investing names from around the world — including Peter Schiff, Bill Bonner and Jim Rickards — to share their insights, knowledge, and strategies for investing in gold and gold stocks in the current market. Today’s session is with Gold Stock Data founder Don Durrett, exploring profitable opportunities in different stages of the mining lifecycle. Register for your FREE ticket here. |

|

| The House Always Wins in the End |

Thursday, 18 August 2022 — Albert Park  | | By Catherine Cashmore | | Editor, The Daily Reckoning Australia |

|

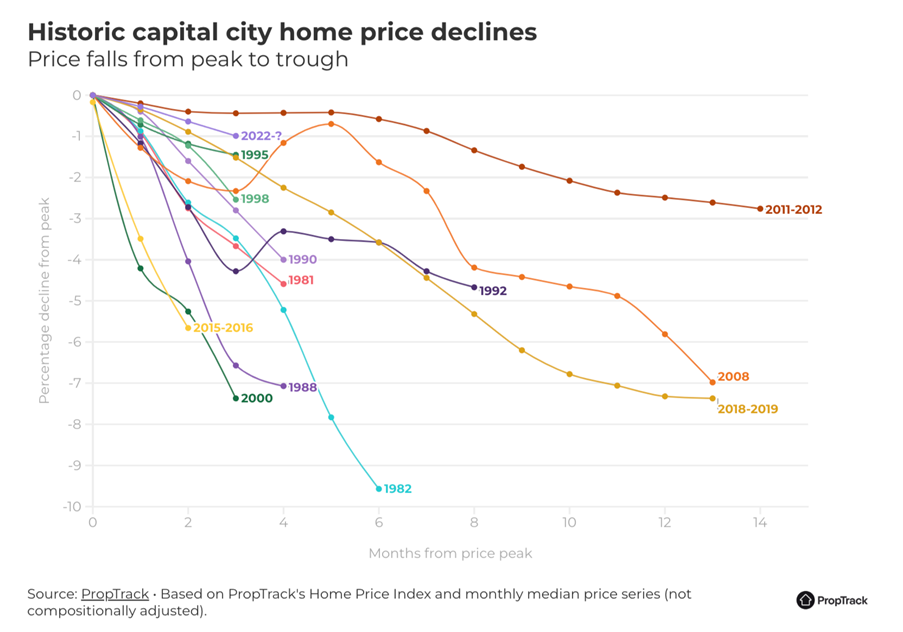

[5 min read] Dear Reader, ‘We expect capital city prices to fall 18 per cent over the balance of 2022 and 2023, before a 5 per cent gain in 2024 as mortgage rates fall’, said ANZ senior economists Felicity Emmett and Adelaide Timbrell this week. To give some context, an 18% *crash* in median values (because that’s what it would be if the forecast played out) hasn’t occurred in the Aussie property market for decades… You can see this on the chart below — it shows capital city price falls from peak to trough since the early 1980s:

Sure, the median can cover a lot.

If an owner needs to sell — and there are no buyers — likely they’ll have to slash the price 10–20% to get a sale.

I’ve seen a few examples of that over the first half of this year, particularly at the top end of the market.

But to get a broad-based drop of 18% in the median capital city house price would require a large proportion of property owners desperate to sell, hitting the market over the period, and nothing to support prices on the other side.

I just can’t see it happening.

A large proportion of households with variable rate mortgages are well ahead in repayments.

We’re not in a period where it’s hard to find employment.

It’s not the GFC.

And let’s face it, those that are subject to increases in rates will do everything they must to avoid default.

Cuts to spending on the one hand — seeking an increase in income on the other.

If you need a job, you can get one.

I would also argue that it’s never been easier for mortgage holders, in an age of technological innovation, to access multiple streams of income.

If some owners require an extra $200 per week to meet rising rates and prevent going into foreclosure, it’s possible to generate it.

I stumbled across this story the other day:

‘Sophie Thomas, 33, rents out her clothes on The Volte and says it has been “such a positive experience” and a good return on investment, earning her $3000-$5000 a month. ‘“I bought a dress for my son’s christening while I was on maternity leave one year ago and I really couldn’t afford it at the time,” she says. ‘I had heard about renting out dresses on The Volte so I uploaded after the christening — the next day I woke up to my very first booking request. ‘Thomas says the money made through renting out clothes is paying for her upcoming wedding. “It’s amazing that the wedding costs are covered from a side hustle and not coming out of our income,” she says.’

The Volte says some users make more than $100,000 a year and the average user earns $1,500 monthly.

And there are a plethora of platforms offering something similar:

- Spare bedrooms can be rented out on platforms such as The Room Xchange — potentially bringing in up to $1,000 a month.

- Caravan and motorhome owners can rent out their vans on Camplify. The platform saying users can earn up to $10,000 annually.

- Online marketplaces such as eBay, Gumtree, and Facebook Marketplace have reportedly delivered some users the equivalent income of a full-time job.

- You can share your car for cash on platforms like Car Next Door for an average of $280 a month.

The platform claims:

‘Some members have turned car sharing into a side business, with a fleet of 10 cars making an average of $103,604 a year… ‘We have several members who rent out multiple items or spaces simultaneously, so the earning potential is huge.’

Then we have the rise of fintech.

New entrants into the space are offering lower fees and more competitive rates than you can access through the majors.

Just this past week or so, news of fintech lender Futurerent hit the headlines.

This time it’s offering landlords up to $100,000 of their rent in advance to either carry out property improvements or buy another property.

With rents rising of more than 10% per annum on the back of record low vacancy rates in some regions. The market is continuing to attract yield seeing investors.

Subscribers to Cycles, Trends & Forecasts know where (and when) this is all going to end.

But right now, it’s fuel that offsets outlandish calls of 18% drops to the median over the next 12 months.

It’s not all ‘doom and gloom’ in the real estate market either.

This week, 27-year-old cryptocurrency casino owner Ed Craven smashed the Melbourne house price record, purchasing a mansion in Toorak for $80 million.

To be clear, though, he didn’t buy a house. He purchased 7,200sqm of prime land.

The property is known as Toorak’s ‘ghost mansion’.

A previous owner — HOYTS boss Leon Fink — had half-built a French Renaissance-style mansion on the block. It has been untouched since.

It’s not Craven’s only purchase this year either.

He paid $38 million for another Toorak mansion in March.

The property, a two-level Orrong Rd home, set on almost 2,000 square metres of land.

Never forget — ultimately, all gains from innovation and technology find their way into land’s price through the cycle.

The house (or rather land) always wins in the end.

Best wishes, Catherine Cashmore,

Editor, The Daily Reckoning Australia

| | By Bill Bonner | | Editor, The Daily Reckoning Australia |

|

Dear Reader, In Bloomberg news is this: ‘“Dr. Doom” Roubini Sees Either US Hard Landing or Uncontrolled Inflation’: ‘“The fed funds rate should be going well above 4% — 4.5%–5% in my view — to really push inflation towards 2%,” the chairman and chief executive officer of Roubini Macro Associates said in an interview on Bloomberg Television.’ That’s it. Those are the choices. Inflate the bubble. Or let it die. Nouriel Roubini says he thinks hopes for a Fed ‘pivot’ — from tightening to loosening — is ‘delusional’. In the near term, he is certainly right. Fed governors are not stupid…at least, not in a conventional way. It took many years of study to become the simpletons they are. And they are still human! Let’s not forget; they don’t like people laughing at them behind their backs any more than anyone else. And now, everyone can see that they made a huge mistake by not raising interest rates sooner. Then, they made another huge mistake by not recognising the threat of inflation sooner…and still another big mistake by believing it would go away like a summer shower. Instead, inflation has settled in…and has been drenching consumers for more than a year. Up to their necks And now, Fed governors must atone…they must make good…they must prove that they are not hopeless morons. How? By getting control of the situation. That is how they will ‘regain credibility’. And that means — as Mr Roubini tells us — getting the Fed funds rate up above the inflation rate. (Point of reference: The Fed, in 1982, put the key rate about 600 basis points…6%...ABOVE CPI to get control of inflation. Currently, the rate is 600 bps BELOW inflation.) The trouble is, the higher the funds rate goes, the more people have trouble paying their debts. The Fed’s ultra-low rates encouraged people to borrow. Now, they’re up to their necks in debt. And most, but not all, debt needs to be refinanced from time to time…which means people have to pay a lot more in interest. Already, from June ‘21 to June ‘22, the typical mortgage payment rose by US$700. All central bankers learn the theory of Keynesian central banking by heart. It’s very simple, based on the Bible story; Joseph interpreted Pharaoh’s dream…in which the latter saw seven skinny cows and seven thin ones…which he took to mean that there were seven years of famine coming. Pharaoh then began a ‘counter-cyclical policy’ of stocking grain during the fat years in order to have something to eat in the lean ones. In the Fed’s version, interest rates are raised during the fat years and lowered when the famine threatens. At least, that is the idea. In practice, the Fed really has no idea what is going on…and being human, Fed governors prefer fat to lean and don’t mind a little legerdemain to keep the pastries coming. That is, they lower rates — even when the economy is strong. You’ll recall that the economy in 2019 couldn’t have been stronger. It was Donald Trump’s turn to play Pharaoh. He said it was the ‘greatest economy ever’. Enter Mother Nature The Fed had been trying to ‘normalise’ interest rates after leaving the fed funds rate ‘near zero’ for far too long. By the time it got up to 2.4%...in 2019…the stock market turned down…and the Fed panicked, dropping the rate down to zero again. But it was not Mother Nature who determined the lean years or the fat ones in the US economy; it was Fed policy blunders themselves. Everybody likes the fat years, especially the elite, whose stocks and bonds go up. And the Fed, an arm of the Wall Street elite, did what it could to make it happen. In other words, the people implementing the counter-cyclical policies were the same people who were tricking up the cycles. It was as if the umpire had run around the bases, slid into home plate, and pronounced himself ‘SAFE’! The Fed could not counterbalance the boom, 2009–21, because it was the cause of it. By 2021, it had been force feeding the economy with cash, credit, and fat-inducing calories for more than a decade. And then, in 2021–22, inflation shot up, the stock market fell, and the economy entered a recession. But the Fed couldn’t provide any counter-cyclical policy to offset the bust; its storerooms were empty! It had already dropped the key rate to zero. And now, contradicting the rules set forth in the Central Bankers’ Handbook, it has to raise rates in order to stop inflation and recover a little of its dignity. And what now? Uncontrolled inflation? Or a hard landing? Which will it be? Our guess: both. A hard landing…and then uncontrolled inflation. But we’ll wait to see what happens, along with everyone else.

Regards,

Bill Bonner,

For The Daily Reckoning Australia Advertisement: Attention: Gold enthusiasts, investors, and speculators…

register now for the FREE gold event of the year Join Peter Schiff, Jim Rickards, Bill Bonner, Don Durrett, and Brian Chu over five days as they explain why you should own gold and gold stocks in the current market… LAST CHANCE TO JOIN TODAY Go here to claim your FREE ticket now |

|

|