| The Beginning of the End Has Consequences |

Tuesday, 25 January 2022 — Gold Coast, Australia  | | By Vern Gowdie | | Editor, The Daily Reckoning Australia |

|

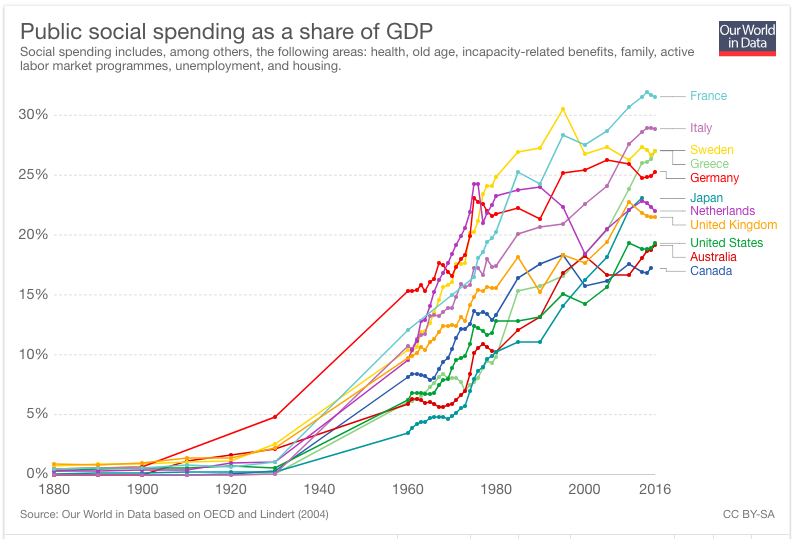

[12 min read] Dear Reader, We’ve seen this ‘beginning of the market end’ movie a few times in recent years. There was 2015. Then came 2018. And, most recently, the short sharp hit in March 2020. Each screening proved to be a tad premature. Courtesy of its central banker benefactor, Wall Street found another gear (literally and figuratively). Is this current case of the jitters the grand finale to the mother of all bubbles? Drum roll, please… Yes, it is. The downward slope will be interspersed with the inevitable ‘buy-the-dip’ rallies. But these are unlikely to be of a lasting nature. This is a bubble that needed bursting. We, as a society, have become too far removed from reality. Crypto pyramid schemes. Meme stocks. Non-fungible tokens. Tech stocks trading on 100 times sales. These are flights of fantasy indulged by people who have lost all bearing on real value. We are headed into a bear market…and it’s likely to be brutal. Trillions of dollars in paper profits are going to be shredded into confetti. Destruction of wealth — on the scale I think we are going to see in the coming years — comes with personal and social consequences. Who is going to foot the welfare bill? A picture paints a thousand words… This rather depressing picture on the steady increase in public social spending (health, welfare, family benefits, public housing) tells you all you need to know about what governments have in store for future taxpayers. Little by little, more of your earnings, savings, and investments are going to be seized to feed this growing monster. Governments, the world over, are embracing socialist agendas. The once Holy Grail of a budget surplus no longer rates a mention. Grandiose vote-buying schemes — financed by central bank money printing — are now the norm. No politician in their right (or, should that be, left) mind would ever talk about lowering public social spending. There’s no way any politician is willing or able to unwind nearly six decades of social conditioning. Three (and possibly four) generations are hooked on some sort of government handout. How much do we think we are entitled to welfare? Remember in 2015 when PM Tony Abbott proposed a GP co-payment of $7? Here’s a quick reminder (emphasis added): ‘The Abbott government’s GP co-payment has been killed off for good with Heath Minister Sussan Ley telling Coalition MPs “we are not pursuing it at all”. ‘Prime Minister Tony Abbott has made several attempts to wind back the widely loathed $7 fee — first announced in the 2014 May budget — in an attempt to mollify public concern.’

Sydney Morning Herald, 3 March 2015 If paying $7 to go to the doctor was ‘widely loathed’, what hope do we (as a society) have of voluntarily undertaking serious reform? None. Zip. Doodah. With the ‘Everything Bubble’ on the verge of bursting and creating an even bigger credit crisis than 2008/09, we are going to see governments (of all stripes) announce all sorts of rescue packages. Rising unemployment. Lost retirement savings. Increased levels of personal and business bankruptcies. All these negative factors will create highly charged political responses…played out for all the world to see on social media. The public pressure on governments to do something — like they did with COVID — will be too great to resist. The last great credit crisis — no, not the one in 2008 — was in the 1930s. That was an entirely different generation with an entirely different mindset. Our forefathers were far more independent and resilient. Government handouts were virtually non-existent, and there were no pouted poses being posted to publicise your woe-is-me plight. The Depression generation just ‘sucked it up’. Accepted their lot and made the best of a bad situation. Not going to happen next time around. No way, Jose. Our entrenched nanny state mentality means the cry will go up for ‘government to do something’. And, believe me, they will do something. But as we know, a government solution is just another (bigger) problem in the making…one that requires an even bigger (more ridiculous) ‘solution’. Doing nothing is not in a politician’s DNA. And, thanks to central banks, the political class has the printing press to finance their most fanciful of social engineering programmes. Quick quiz…who wrote this and when? ‘The welfare state is nothing more than a mechanism by which governments confiscate the wealth of the productive members of a society.’

Never a truer word was written by…Alan Greenspan in 1966. Oh, the irony. Welfare payments are a wealth transfer mechanism…taking from the productive to give to the unproductive. That sounds harsh in this new age ‘touchy-feely, every kid gets a prize’ world we live in…but it’s the brutal, ugly truth. In addition to the money being doled on social spending, there’s the cost of the bureaucracy to administer these payment schemes. Paying for past and present government vote-buying initiatives is a very costly business. For the long-term good of society, we need to wind back the welfare gravy train and tighten up the criteria on who qualifies as a worthy and genuine recipient of taxpayer money. Oh, how I dare to dream. Advertisement: Worried about a market crash? You SHOULD be… This is no ordinary uptrend. According to the findings in this just-published research report, it’s the most dangerous collection of overpriced assets in the history of mankind. Click here to read ‘Four CODE RED Investments to Sell Now’ |

|

Productivity will be encouraged. People will become more self-sufficient and less reliant on government. More money in the taxpayers’ hands and less in the government coffers will result in a better allocation of resources. There would be less bureaucracy. All positives for a stronger economy…but there is one rather large obstacle on the path to this hoped-for economic nirvana. The political class, the bureaucrats (who are too incompetent to make it in the private sector), and the grafting industries that have profited greatly from being on this wealth transfer gravy train will never put society’s intertest above their own. What a different world it might have been if Greenspan had remained fast to his principles…then again, if he had, he most probably would not have been appointed chairman of the US Federal Reserve in 1987. Greenspan’s long tenure as Fed chair shows us how well he learned to play the political game. Better than anyone before or after him. Greenspan entrenched the Fed’s interventionist culture…openly supporting asset prices by making credit freely available. The Fed’s policies — indirectly — provided the government with the tax revenues to continually expand welfare programmes. Greenspan’s blatant 180-degree about-face is why the ballooning welfare problem will never be addressed voluntarily. Anyone who dares to endorse the Greenspan view of 1966 cannot survive in politics…the system will grind them into dust. There are just too many vested interests. What cannot be achieved voluntarily is therefore destined to be done involuntarily. In due course, the system will collapse under its own weight of over-promised entitlements. That’s not going to happen anytime soon. Old habits die hard. When the next Great Depression hits (in the coming years), central banks will print money (on a scale we have never seen before) to finance more handouts and bailouts. Be prepared for the government to turn over every rock looking for a tax dollar to fund the interest bill on ballooning public sector debt. With its lower tax regime, superannuation will still be the most attractive savings vehicle. But there’s only so much blood the politicians can extract before the tax-paying patients become anaemic. That’s when ‘adjustments’ to welfare programmes will be made. And that’s when boomer retirees are going to be in the crosshairs of millennial politicians. Those entering retirement and expecting an indexed Age Pension in the years to come should think again. The concept of paying people an increased amount each year for 30 years or more is not sustainable. Tighter rules will be implemented. Increase in the pension eligibility age. Tougher income and assets tests. The family home to be included in the Asset Test. My suggestion is to look at building resilience and independence into your retirement plan. In anticipation of a significant reversal in market fortunes, adopt a more defensive asset allocation. Be prepared to wait patiently for the market to exhaust itself on the downside. Then, when the market offers up a low-risk/high-reward proposition, consider increasing your allocation to beaten down equities. In my opinion, we are at a major turning point in market history…think pre-October 1929. The decisions retirees and pending retirees make in the near term, could have life-long repercussions. With the prospect of a greater percentage of society becoming more dependent on government largesse, it’s never been more important to have financial independence. The less dependence you have on the system, the greater the freedom you’ll have in the longer term. Regards, Vern Gowdie,

Editor, The Daily Reckoning Australia

| Why We Decided to ‘Go Private’ after 40 Years of Public Spectacle |

| | By Bill Bonner | | Editor, The Daily Reckoning Australia |

|

Hallelujah and pass the Guinness! Like the UK and Spain, Ireland has decided to go back to normal. COVID restrictions have been almost completely abolished. And on Saturday night there was general rejoicing. Curfews were lifted…and people gathered in pubs to celebrate. It was like the end of Prohibition in the US, with laughter and singing. Young and old were happy to be free at last…and able to raise a glass together without the feds threatening to arrest them. Ireland followed a strict program of masking, vaccinating, and contact tracing. Almost everyone is vaccinated. And it’s an island…which makes it a little easier to keep out unwanted visitors. But that didn’t stop Omicron from coming ashore. Cases soared. But so few died that the Irish government came to its senses, and saw no benefit in continuing to fight against it. The war is over! Meanwhile, back in the US…the war continues. What was it Lenin said? ‘There are decades where nothing happens and there are weeks when decades happen.’

What a week. And what a weekend! The Nasdaq is off to its worst start since 2008. Back then it fell 13.6% in the first 14 trading days of the year. By Friday’s close it was down more than 11% year-to-date here in 2022. If things keep tracking this way, it will be the worst January since the inception of the index in 1971, according to Dow Jones Data. There is plenty of pain to go around. Look at the chart below, sent by our colleague Dan Denning over the weekend. Warren Buffett (the compounding tortoise) has caught up with Ark Invest’s Cathie Wood (the hare) and her racy Ark Innovation ETF [ARRK]. Ark shares sinking fast Both Buffett and Wood are still up since the beginning of the pandemic in the first quarter of 2020. Both benefited from the Fed’s war against normalcy…with a huge expansion in the Fed’s balance sheet and much lower interest rates. The big question now is: what next? If it’s a ‘super bubble’, as Jeremy Grantham, the 83-year-old founder of Grantham, Mayo, Van Otterloo & Co, says, the major indices may fall by 50% or more. Grantham’s maths is roughly the same as ours. About US$35 trillion in ‘wealth’ will be wiped out. In other words, the real bear market hasn’t even begun. Real bear markets last months and years, not days and hours. And by the time they’ve done their work, no one is trying to find the bottom anymore. At the bottom of a bear market, no one wants to talk about innovation, NFTs, or decentralised finance. Setting sail for greener pastures Grantham likes cash, gold, silver, and some emerging market stocks and value stocks that have not been bid-up to ridiculous multiples of sales in the last two years. We think he’s onto something. And so does our new Investment Director, Tom Dyson. But perhaps we should back up a second. Much has happened in the last month since we set out on a new venture. It’s probably time for a fuller explanation. It’s not always clear to us what we’re trying to do…it may not be entirely clear to you, either, especially if you’re new to these Diaries. We began writing in 1998. Sometimes, these daily missives were hard to write. They must have been even harder to read! Because we’re like travellers who never know exactly where they’re going. Instead, we look, we wonder…what’s happening? Why? Where does it lead? Sometimes the questions take us down blind alleys and waste our time. Often, they simply lead to more questions. Only occasionally do they guide us to useful insights. Rarer still, to actual wisdom. The benefit of experience We started our first newsletter, International Living, in 1978. In it, we hoped to show Americans how to retire overseas. It was a dream then. For many thousands since, it’s become a reality (and for some today, an urgent priority). More than 40 years later, in the home stretch of our career, we are beginning a new project again. Fortunately, writing about money is one of the few métiers where age is actually a benefit. After all, you have to be over 70 to have lived through, as an adult, the inflation of the 1970s. You have to be at least in your 60s to recall how Paul Volcker stopped it. Besides, as you get older, you may become more vulnerable to COVID, but you become more resistant to claptrap. You remember the WIN buttons…the lime-green leisure suits…and the Vietnam War. You’ve embarrassed yourself more often than you can remember…and you’ve heard too many something-for-nothing claims, seen too many new tech promises that didn’t work out, and voted for too many disappointing politicians; a grain of salt is no longer enough…you need tons of the stuff. We bring this up because we think we are approaching a period of Peak Disillusion — when the silly pretensions of the governing class create a disaster for everybody. A good dose of geezer cynicism may be the only way to survive it. Many of the trends we’ve been following for decades seem to be both accelerating and converging at the same time. The ‘new’ dollar — without gold backing — was introduced more than 50 years ago. When it came out, the old-timers preached doom. Now, we’re going to see that they were right. No pure paper money has ever survived a full credit cycle. Our guess is that this dollar will be gone when interest rates reach their next top. Will it be replaced by something else? Just last week the Fed released a long-awaited research paper on a central bank digital currency. Is it coming soon? Everything’s happening faster than it used to. The four stages of work Looking back over our half-century of work, we see different stages. First, we thought we could change the world. Young people often think they have the answers; we did. And we were worried, in the early ‘70s, as now, about the growth of government. The central competition in public life is not really between Democrats and Republicans or liberals and conservatives. It is between those who go about their business…helping each other…providing goods and services to each other…building wealth and families…and those who want to stop them. It is the difference we described in much more detail in our book, Win-Win…or Lose, between those who make…and those who take, between those who get what they want by honest, consensual exchange and those who use armies, sanctions, laws, and regulations. It is the difference between violence and persuasion. Still in our 20s, we were naïve and foolish. We believed the growth of Washington and the proliferation of laws and regulations was some kind of ‘mistake’. People just failed to realise that ‘win-win’ was a better way to go. But after seven years in Washington, heading up a group called the National Taxpayers Union, we finally had to face facts: a lot of people prefer power to prosperity…and that includes almost everyone within the DC Beltway. Information is not wisdom So, in the second chapter of our career, we left ‘public interest’ and decided to focus on private interest. We couldn’t change the world, we reasoned, but at least we could help people get through it…and make some money for ourselves doing it. We were supremely lucky. It was just the beginning of the financialisation phase of the US economy. In 1971, the feds had switched to a paper money system, unconnected and unrestrained by gold. It was off to the races. Everyone wanted to know what horse to bet on. We were, however, woefully unprepared for our new role. We didn’t understand much about economics or investing. So we teamed up with people who did. Gary North, Mark Hulbert, Adrian Day, Doug Casey, Jim Davidson, John Dessauer, Porter Stansberry, Steve Sjuggerud, Alex Green, and many others. Sometimes they were right. Sometimes they were wrong. But we were always learning. And we are grateful to them all. Then, in the late ‘90s, came the third stage of our career. The internet arrived. People said it would make ‘information’ available — free — to everyone. That would put us old-fashioned newsletter publishers out of business, they said. But ‘information’ is worthless…less than worthless…without context…trust…training…preparation…circumstance and all the other things that give it value. ‘Imagine Napoleon on the retreat from Moscow’, we invited readers. ‘His soldiers are freezing to death. Starving. Getting slaughtered by partisans. And then…as if by some miracle…someone hands him the plans for building a nuclear bomb! What value would that have had? Zero.’

Our point was that the precise ‘information’ you need, precisely when you need it, is extremely valuable. Otherwise, it’s just excess baggage. We went on to speculate that with the build-out of the internet, ‘the world may soon be stuffed with information…and starved for wisdom’. In the following years, instead of fading away…our business boomed — thanks to the internet. Investors gorged on ideas, recommendations, revelations…about new tech breakthroughs…trading techniques…cryptos…pot stocks…and much, much more. Many of these turned out to be astonishingly profitable. But your editor, who began writing a daily ‘blog’ in 1998, was a wet blanket. He doubted that these innovations would produce lasting wealth — after all, what did they produce at all? Many provided neither products nor services…and many lost money, year-after-year. As to the new tech, he urged caution. In retrospect, his counsel turned out to be both good and bad. He eschewed investments in dotcoms…even in the most successful of them of all — Amazon. He wondered aloud if the whole ‘information revolution’ was anything more than a time waster. And he ridiculed many of the most sacred tenets of tech believers…including the doctrine that new technology always means progress and that progress will free humans from work, thrift, and sin. Trade of the Decade On the other hand, his one, very simple ‘Trade of the Decade’ — sell stocks, buy gold — turned out to be the best trade of two decades. Gold, at the end of the 1990s, was trading at US$282 an ounce. The Dow was just over 11,000. Since then, gold has gone up about six times. The Dow is only up three times. Our current Trade of the Decade, unveiled around this time last year, is doing well too. The ‘short’ side isn’t complicated: the US dollar. The whole worldwide bubble is full of dollars. Stocks, bonds, real estate — everything is quoted in dollars. And while the Fed will be desperate to keep asset prices from crashing…it can only hope to do so by ‘printing’ more dollars to boost them up. It’s the ‘Inflate or Die’ trap. Either asset prices decline…or the dollar does. The dollar will be sacrificed, we believe, to try to save a corrupt and doomed financial system. Too much noise, not enough signal But now, we see a bigger challenge ahead…and the fourth and final lap for our career. After a quarter of a century of burgeoning internet-based investment advice…and all manner of opportunities — NFTs, cryptos, tech breakthroughs galore — investors are swamped by ‘information’ and opportunities. But wisdom? It seems to have disappeared. Where it still appears in residual clumps, like survivors after a worldwide plague, it is furtive…fearful…and almost ashamed of itself. And it is completely upstaged by the gaudy claims of the tech futurists. One says a new ‘disruptive’ tech will bring 10,000% gains. Another says a pharma breakthrough will allow children born today to live to 200 years old. Still another claims you can double your money overnight. And maybe they’ll be right! But we have our doubts. Nature is not so promiscuous as to give out her favours to every Tom, Dick, and Harry who buys a newsletter subscription. She knows that real progress…and real wealth...require real work, real investment, real reflection, and real self-discipline over what is generally a really long time. So that is our goal. There’s a lot of work to be done! We’re using a new platform because it lets us focus almost entirely on writing and researching. That’s why you don’t find any offers for other services in these letters. All we have to offer you is ourselves…our research…our guesses and hunches. Sometimes right. Sometimes wrong. And always in doubt. But like any new project, there are a few bumps in the road. We’re working on them. Thanks for your patience. In the meantime, we’ll keep our eyes on the big prize. Yes, we search for the rarest and most precious thing in the financial world — wisdom. And while we may not find it, it won’t be for lack of trying. Until next time, Bill Bonner,

For The Daily Reckoning Australia Advertisement: A $4 trillion opportunity for Aussie investors… Stocks, property, and commodities have all soared since the pandemic. (In August 2021, property prices rose at their fastest annual rate since 1989!) But according to two of our forecasters, this is just the start of a much bigger opportunity…one that could transform Australia and put a total of $4 trillion in smart investors’ pockets. Here are their five moves you can make now to help take advantage of this opportunity. |

|

|