I write these letters primarily for investors, both individual and professional. We all have a responsibility to someone—ourselves, our families, our clients—to make the best possible decisions. Investing can be fun, but it’s not a game. It is serious business, and we should approach it that way, not as seat-of-the-pants guesswork.

Today I’ll pick up on the “signal vs. noise” theme that David Bahnsen shared last week. I think that was one of the most important letters that I have written in a while. You can read it here if you missed it. I firmly believe keeping that distinction between investment noise and signal clear in our minds is the key to successful investing. But it’s also incredibly difficult… which is why we need constant reminders.

This week the news is about the Israel-Iran conflict. It’s terrifyingly real for those in the crossfire, while we who are safe naturally wonder what it means for us. As investors, we think about the economic and market effects. But are we seeing signal or noise? I argued last week that for the vast majority of investors, it should be noise. But in the large amount of reading I do, I see others who have different perspectives.

My rather famous writer/trader/hedge fund guru friend Doug Kass (who runs the well-known hedge fund Seabreeze Partners) mentioned how one of my letters about the SIC gave him pause:

“Two weeks ago, I read (as I have for a number of years) John Mauldin's luminous weekly commentary in Thoughts from the Frontline in which he summarized some of the comments from his annual Strategic Investment Conference. (Run, don't walk to read Thoughts from the Frontline—subscribe, it's free!)

“John has been a great pal of mine for several decades throughout which I have read his musings in detail and with interest. I was initially attracted to his writings (and thoughts) because of his facts-based market and economic analysis. I particularly admired his objectivity (and ability to react to changing conditions and trends), common sense, logic of argument, and deep dives.

“What caught my eye was his May 31, 2025 issue entitled “Bullish Highlights” in which John highlighted the generally upbeat equity market perspective that permeated his conference (as “pessimism is decreasing”).

“A vivid example was (a historically skeptical) Felix Zulauf, a former Barron’s Roundtable member and Swiss money manager who expects a move to 7,000 in the S&P Index:

“So, if somebody puts a gun to my head, I would say on the S&P 7,000... and then 9,000 again thereafter." —Felix Zulauf

“As I am at the polar opposite of Felix (as I am a short-term bear), I thought after reading Felix's musings, that if he is bullish and sees equities going to new highs, I should pay heed to him. With Felix joining the herd's bullish chorus, I reexamined, over several days, (as John has taught me to do over the years) my ursine market view.

“Despite Felix's apparent bullish turn and after that reexamination (following my second time viewing his SIC presentation) I remain stalwartly negative—and I have concluded that (what I would describe as) The Bull Market in Complacency may soon come to an abrupt end.”

Doug then went on to note [emphasis mine]:

“The Israeli/Iran conflict (now into its fourth day) is yet another in a long list of uncertainties that investors face. And with a starting point of a 22.5-times price-to-earnings ratio, investors are underappreciating and underpricing risk:

- We face the highest geopolitical risks in many decades (which will not be resolved quickly).

- We face the largest level of social and political risks in the US since the Vietnam War.

- We face the greatest chance of “slugflation” (slowing economic growth and sticky inflation) since the 1970s.

- We face the biggest threat that the US dollar and capital markets will no longer be a “safe haven” in modern history.

- We face the greatest debt load and deficit ever—and neither party seems to favor any fiscal discipline whatsoever.

- We face the largest capital spending spree in history (on artificial intelligence) though the return on that investment is less certain.

- We face a viable alternative to equities in fixed income (for the first time in 15 years) as bonds present an equity-equivalent yield with limited risk and volatility.”

I would add tariff and trade policies. And not just US but global trade. It is clearly shifting… but to what? This is not just a US-driven or a US concern. The pressure is everywhere.

Doug thinks all this will add up to a bear market—though, to be clear, he says later on he intends to be cautious with short trades because the market remains so strong.

Doug is a trader of stocks. He runs a long/short hedge fund. He watches markets all day, every day, looking for profit opportunities that may last only a few days or weeks. That’s not just a hobby. It is a full-time job to which he gives his full-time attention. Most of us have other concerns and aren’t in a position to do that. We are investors, not traders. They aren’t the same thing and, whichever you are, it’s critical to stay in your lane.

For trading Doug, the Israel-Iran conflict is a signal. Doug sees signals in lots of other things that I would consider noise for my investment style. And you should too.

A lot of smart people are sketching out what the latest Middle East conflict will mean. It could go many different directions. I expect little global economic impact as long as oil shipments keep flowing. The outlook could worsen quickly if tanker ships start getting attacked. Insurers will effectively close the Persian Gulf, no matter what anyone wants.

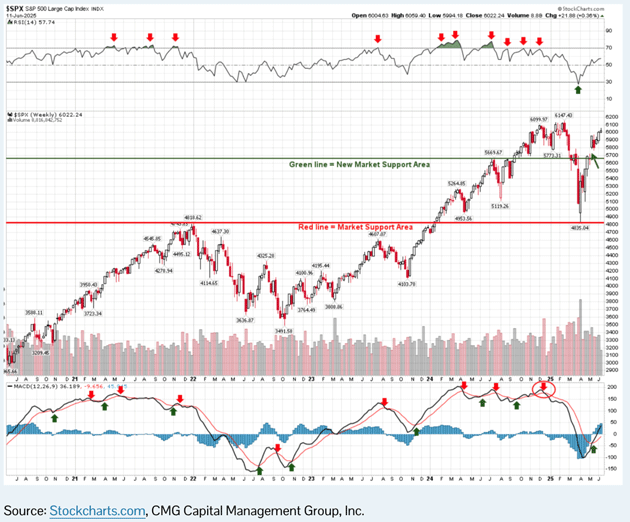

Now, let’s talk about Felix Zulauf. Felix is also a trader. He uses quite a bit of technical analysis. I don’t have permission to use his chart, but here’s one that’s similar. It uses Moving Average Convergence/Divergence (MACD), a trend-following momentum indicator.

Source: CMG

The use of these charts and scores of other technical indicators like them can get quite sophisticated. Basically, and I used it in my early days, you can chart entry and exit points by moving averages. The consolidation of the market and other factors make this far more difficult today than in the 1990s and 2000s. I seriously ran market timing portfolios and invested in them in the late ‘90s and early 2000s and did fairly well. But for a variety of reasons, those systems began to show cracks, and for once in my life, I actually got out in time. I had one large institutional investor tell me that he had never had a money manager close his fund when he was making money. He really wanted me to continue. But my personality just doesn’t lend itself well to actually managing money. I made the right call.

Felix’s latest letter is titled “The Easy Money Has Been Made.” Felix is more concerned about getting the trend right than actually predicting a number. He can change on a dime if the trend does. He thinks we are getting close to what he calls the medium-term top. But he doesn’t expect a true crisis until much later in the decade. On that, we agree.

For Felix, the trend is bullish. He thinks the US will continue to run large deficits and maintain an easy money policy which will put wind in the sails of a bull market. Maybe. I think the market at 22.5 earnings, largely concentrated in a few stocks, is problematic. Do I think there are individual stocks that could go up from here? Absolutely. But right now, friends don’t let friends buy index funds.

There are literally thousands of Dougs and Felixes out there. There is a 99% probability you are not one of them. You can invest with them (or others like them) if you like. If their strategy makes sense to you. But don’t think you can trade with them.

For the last two years, I have participated in a weekly call with 40 to 45 individuals. These are mostly traders/operators/large investors, with some geopolitical analysts thrown in. It is a well-run, thoughtful exchange. These are serious investors, most of whom run their own money. They spend a great deal of time studying companies and industries. They openly talk about their portfolios. Those who were long or short stocks or bonds (or whatever) have specific reasons for doing so. They really don’t get long or short “the market.”

While they are interested in everything, they are more interested in the details of their investments. Because many of them are short-term, the difference between signal and noise is different for each of them, as it should be for you.

So, yes, if you’re willing to put in the effort and spend months and years gaining experience in very specific markets, you can be one of them. Just use an abundance of caution starting out.

Today’s (often younger) investors frequently say, “There is no alternative” (TINA). That is a silly notion. I’m telling you there are alternatives.

We should also note that markets can go through long stretches that are neither bullish nor bearish. They can also go sideways. In fact, an extended flat market can wring out excesses just as well as a bear market, just not as quickly. I wrote in late 1999/early 2000 that I thought the S&P would be flat for the decade. I was considered too bearish. It turned out I was right. Probably by luck, but the historical data we were looking at suggested that valuations would change over the next decade. A buy-and-hold index fund mentality through two recessions didn’t work. Yet, after 2009, it clearly did. Things change. I think we are more like the former period than the latter, today. By the way, there were many things that did work in the 2000s. There were lots of alternatives.

Furthermore, “the market” isn’t our only investment option. It is true that simply throwing your money into the S&P 500 or Nasdaq 100 has been hard to beat for many years now. If that’s what you mean by “the market,” then of course you see no alternatives.

But, in fact, the financial markets offer a rich tapestry of interesting companies and sectors. “There is no alternative” is nonsense. There are always alternatives. At any given time, some will look better than others. Large-cap technology has been in that position for a long time but hasn’t always owned it. Things change.

If the broad indexes enter a sideways pattern, some stocks will still perform well. They will probably attract interest quickly, which means the highest gains will go to the buyers who beat the crowd. That’s where you want to be. But how do you know where to go?

You have two options. The first is to stop being a crowd-follower and develop the skills and intuition needed to identify future winners. This is hard because, almost by definition, those future winners don’t presently look like winners. Many will look like losers, in fact. Your research will quickly find that many smart people say to avoid them like the plague.

That’s not an accident. The fact that so many people are saying, “Don’t buy this stock,” is a prime reason its price is so low. And, quite often, a low price is low for a very good reason.

But what I’m describing here is “value investing,” the method Warren Buffett, Howard Marks, and numerous others have followed to great success. They win not by selling high, but by buying low. This takes courage and an incredible amount of patience, plus a rare ability to ignore critics.

Adopting a value approach in today’s environment has the additional advantage of putting you in stocks that, if we enter a bear market, may not fall as much as the well-known tech names. Their valuations are already in the reasonable zone, if not lower, so they are closer to the bottom.

Choosing which investment strategy to use is incredibly important. Whatever strategy you adopt, the key is to stick with it. An imperfect strategy you can comfortably follow is better than a fully optimized one you will abandon at the wrong time.

For many and maybe most investors, following one of these more difficult methods is easier with a professional manager. Aside from the fact they are probably better equipped to do the necessary research, a good manager will help you hold on through the inevitable rocky times.

(This assumes, of course, you pick a good manager, which has its own challenges. The personable one, who takes you to play golf or dinner, may talk a good game yet not be the best choice.)

Again, there are basically two things that can happen to a market as richly valued as this one. One is that the momentum fades, but a crash doesn’t follow. People who grew accustomed to buy/hold/forget won’t like it but will be slow to give up.

The other possibility is a true bear market, in which valuations fall back to normal and then fall some more. No one will like this, except maybe value investors who will suddenly see opportunities everywhere.

Typically, bear markets don’t happen outside of a recession. For decades, the most reliable indicator/warning for a recession was the inverted yield curve. It has not just been wrong of late, but really wrong. And, while I can see weaknesses in the economy in numerous places, it is more like a softening of fairly good data or a correction in an overvalued portion of the economy.

For instance, housing prices in many markets are beginning to fall, and of course, that correction varies by region and location—not a large amount, given that housing prices have risen precipitously over the last few years. It is reasonable for prices to come back to where buyers can be found. The same can be said in lots of different markets.

But watching data soften is different than saying, “This one thing always happens before a recession.” If there was such a thing, we would all know about it. And mostly, the “one thing” that the writer says is a clear recession indicator has predicted 17 of the last 6 recessions. It might make for an interesting, sometimes breathless, piece of writing, but it truly is noise. There are literally hundreds of statistics and indicators that will actually go down before or during a recession. But before a recession, the same indicator will go up and down many times without giving any meaningful information. It’s just noise without a signal.

All that being said, I don’t think the business cycle has been repealed. And while recessions are less frequent, they are still going to happen. That is why your investment style, whether short-term or long-term, needs to take recessions into account.

Now, pinpointing when a recession and a bear market will happen is hard to say. The S&P 500 just had a correction and is now almost back to the prior peak. If it fails to move higher, we will have a “double top” which some technical analysts usually see as a bearish sign. We’ll see. I, for one, am happy to have my equity allocation mostly with David Bahnsen’s firm, which I think is well-positioned for what I see in the coming years. You have your own decision to make. For his equity portion, he chooses to use companies that have grown their dividends every year over 20, 30, 40 years and are a good value today.

But I know a lot of you actually want to run your own portfolio or those of your clients. Kelly Green, the editor of Yield Shark, our first Mauldin Economics letter besides my own, does an outstanding job of identifying solid dividend-paying companies and combining them into a smart, actionable portfolio.

She’s hosting a live event on July 10, where she’ll walk through the core principles behind her strategy, including how she balances high current yield with long-term income growth.

If you prefer to pick your own stocks, Kelly is a great choice. The live event is free and you can RSVP and submit your questions in advance here, inside her Dividend Digest Community.

I write this personal section at the end of each letter to let people know what’s going on, but lately, it seems to be a version of Groundhog Day. The only actual trip I have firmly scheduled is to the West Coast Fishing Club in late August with over 30 of my readers. It sold out fairly quickly.

As I keep saying, Dr. Mike Roizen and I are opening longevity clinics here in Dorado Beach, West Palm Beach, and Columbia, Maryland (DC) in the coming weeks. I will tell you when they are actually open and can take clients.

I am busier than I’ve ever been in my life, and I am trying (struggling) to find time to learn to incorporate AI into my daily routines as I know it’s going to be important. Plus writing, reading, and research. And the gym. I have this fantasy that things will slow down but it’s not happening yet.

Ironically, much of what I am doing is making me interact with younger generations and I find that exhilarating. Well, most of the time.

I actually can’t imagine that I would have the time to personally research stocks and manage a portfolio with everything I’ve got going on. I am perfectly happy to delegate. And while AI and robotics promise to make us more efficient, what I really need is a clone. Or two. David Brin’s sci-fi Kiln People comes to mind.

And with that, I will hit the send button. You have a great week!

Your needing more help analyst,