For years, the whiskey world rode a wave of hype — booming demand, soaring valuations, and a gold rush mentality around everything from limited-edition bottles to aging casks.

But the buzz is starting to fade, and what’s left behind is a market grappling with the consequences of overconfidence.

While premium whiskeys are still in demand, volume is down. People are paying more per bottle, but they’re buying fewer bottles overall. And while Asia fuels growth, whiskey shelves (and warehouses) are still overflowing.

Add to that a slew of whiskey investment platforms that have gone bust, and you start to see the cracks in the foundation.

Today, we’re breaking down the state of the whiskey market; what's happening, what it means for alternative investors, and where we go from here.

Let’s go 👇

❖ Keep more of what you earn with Gelt

If you’re not proactively planning your taxes, you’re probably overpaying.

Gelt is a modern tax strategy firm built for people with complex financial lives. Think equity comp, multiple income streams, K-1s, crypto gains, private deals — all the stuff traditional accountants tend to fumble.

How it works:

Strategic planning to reduce your future tax liability

Ongoing guidance as your income evolves

White-glove filing done by expert CPAs

Year-round access to an actual team — not just a guy in a polo come April

They’ve already helped hundreds of clients shave serious dollars off their tax bills — and they’re now opening the door to more.

If you're a founder, fund manager, or investor making six figures or more, Gelt could be one of the most valuable relationships you form this year.

The first thing to understand about the whiskey industry is the shift toward premiumization.

Premium whiskeys are in vogue, driven by the rising Asian middle class, influencer marketing, and a shift towards “drinking better” — especially with younger drinkers in the West, where 54% of consumers favor premium drinks versus 35% of older folks.

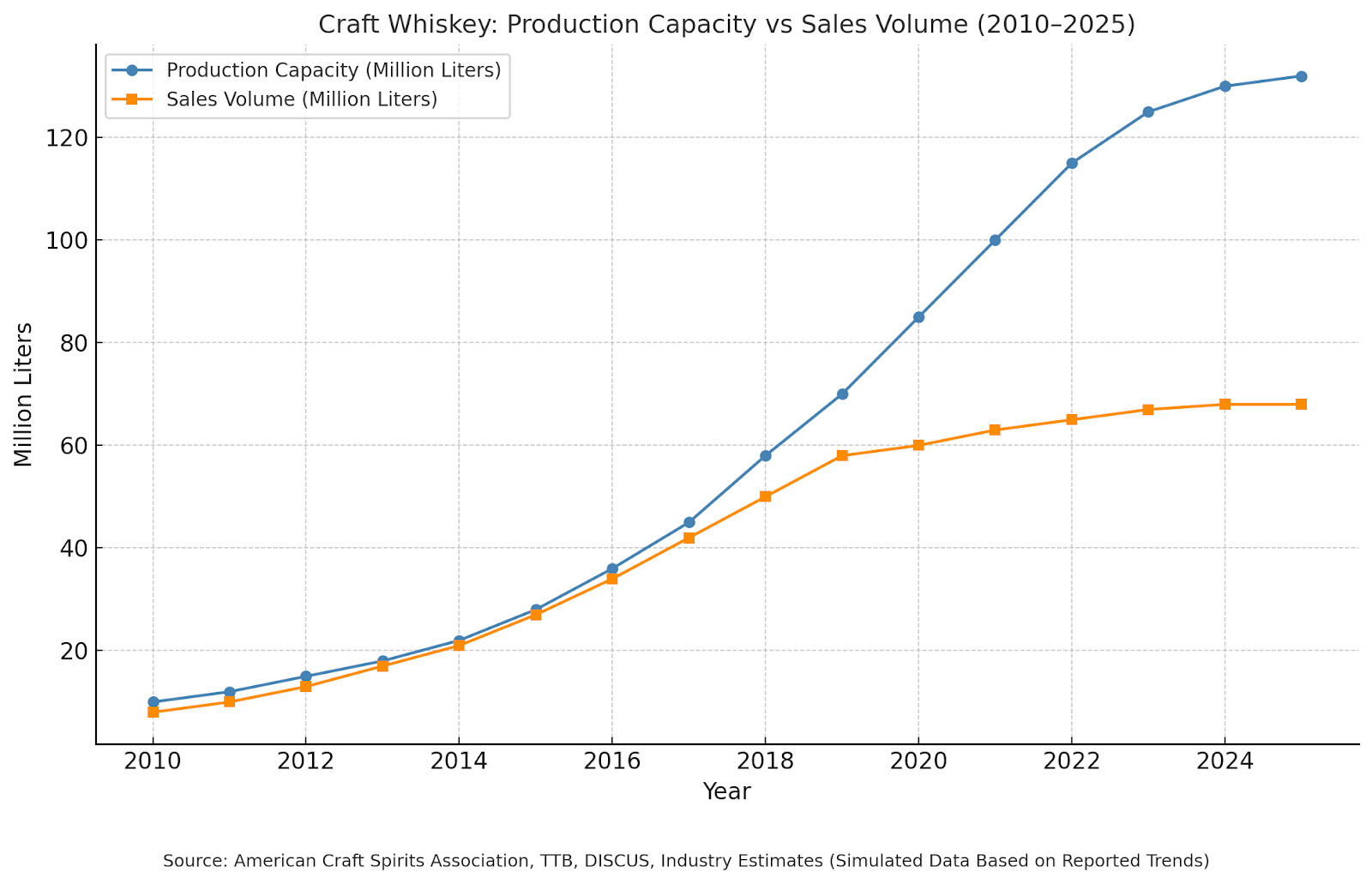

But there’s a catch: whiskey volume growth is flat or declining. So people are spending more but buying less.

Barrel bottlenecks and broken assumptions

Whiskey needs time to age. But barrels, the vessels of that time, are in short supply and are getting harder to come by.

Lumber shortages, delays at cooperages, and even climate change are driving up costs and making long-term planning harder.

But the bigger problem is pure supply vs demand. Warehouses are full, but there’s a growing mismatch between what distillers have and what the market actually wants.

Today’s inventory glut was created based on outdated demand assumptions. As the Kentucky Distillers Association notes, production is up 600% since the turn of the century and 200% in the last 10 years. But volume hasn't kept pace.

Distilleries with strong cash flow and in-demand products can afford to wait things out, aging their liquor nicely until the market recovers. But smaller or overleveraged producers won't be so lucky.

Whiskey's next billion customers: China and India

Growth today is dominated by two countries — India and China — which are the holy grail for whiskey growth.

China's gift-giving culture and appreciation of craftsmanship + rarity have driven demand for the most expensive and collectible whiskey bottles.

Meanwhile India boasts high urbanization, a middle class growing at a whopping 6.3%/year, and rapidly rising disposable incomes.

And don't forget the new free trade agreement with the UK, which means Scotch whisky in particular should continue to rise in popularity with Indians.

The landmark UK–India Free Trade Agreement signed on May 6, 2205 includes a huge reduction in import duties on Scotch whisky. Indian tariffs were halved from 150% to 75% immediately upon implementation.

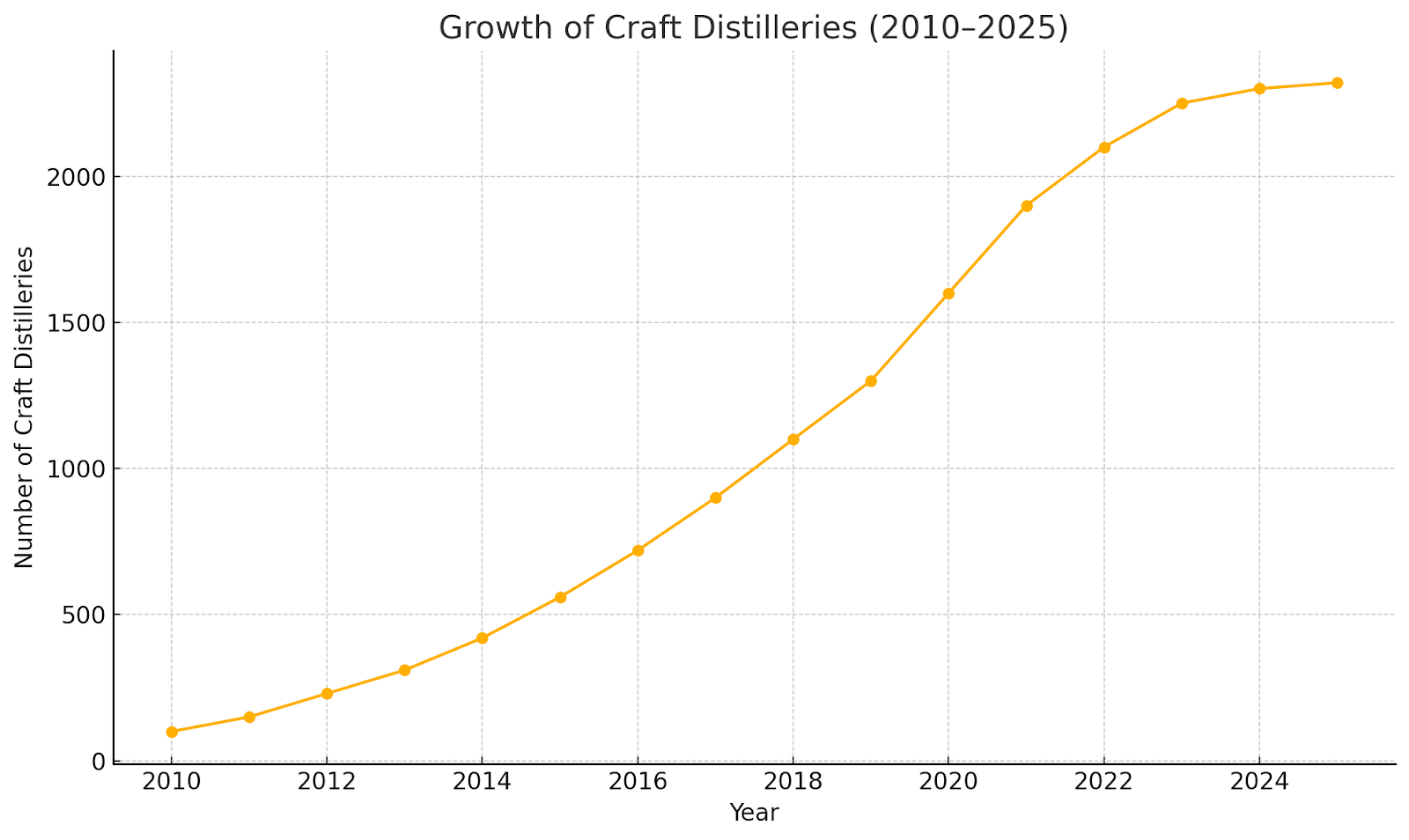

Craft whiskey may be hitting a tipping point

Before it started to plateau, the US craft whiskey boom was one of the biggest alternative investing stories of the past 10 years.

It started out similar to the craft beer movement, driven by regional identity and a desire for quality. But it has become an oversaturated landscape littered with "zombie brands" facing tough questions about survival.

Today, the craft whiskey market is crowded as hell. With limited shelf space and brand fatigue, we expect to see a ton of consolidation, roll-ups, and the quiet disappearance of underperformers.

Not all whiskey brands make their own juice

To examine the rise and fall of the craft distillery, we should pay particular attention to what are known as NDPs, or non-distilling producers.

Think of NDPs as fashion brands that don’t make their own clothes. They don’t own a factory, but they know style.

Instead of sewing garments themselves, they buy high-quality clothing from established manufacturers, then add their own flair — maybe a cool logo, new buttons, or fancy packaging — and sell it under their brand name.

In whiskey terms, NDPs buy aged whiskey from big distilleries, tweak it (maybe finish it in a unique barrel), give it a catchy brand and story, and sell it as a premium product.

While this strategy can definitely succeed, major distilleries are increasingly opting to release their own aged product directly at improved prices.

Age-stated releases like this Buffalo Trace Eagle Rare 12-year bourbon undercut NDP offerings and deliver directly from the source.

Ironically, these fairly priced distillery bottles often fetch much higher prices in secondary markets.

When a high-quality bottle is released at a reasonable MSRP, it becomes a target for collectors, driving scarcity and price appreciation. (In the case of the Eagle Rare 12, some secondary market prices have exceeded $500 — 10x the MSRP!)

Transparency in the secondary market

Since aftermarket prices are all over the place. How do you know if you're paying a fair amount?

This is where platforms like BAXUS have become critical. They give you a super clear view of how many bottles are in circulation, and what bottles are actually selling for. (For you vinyl lovers, think of it like "Discogs for whiskey.")

This lets you acquire bottles at a fair value based on real-time data, and gives producers terrific visibility into aftermarket demand.

BAXUS shows you what individual bottles are selling for at auction houses, as well as their own platform. You can see here that a bottle of Buffalo Trace Eagle 12-year bourbon is selling for around $70 -$95.

Transparency is at the heart of everything BAXUS does. Historically the growth of markets is directly linked to transparency. So the best thing that can happen to consumers and collectors alike is more willing players bolstering an ecosystem built on trust. – Tzvi Wiesel, Co-Founder and CEO of BAXUS

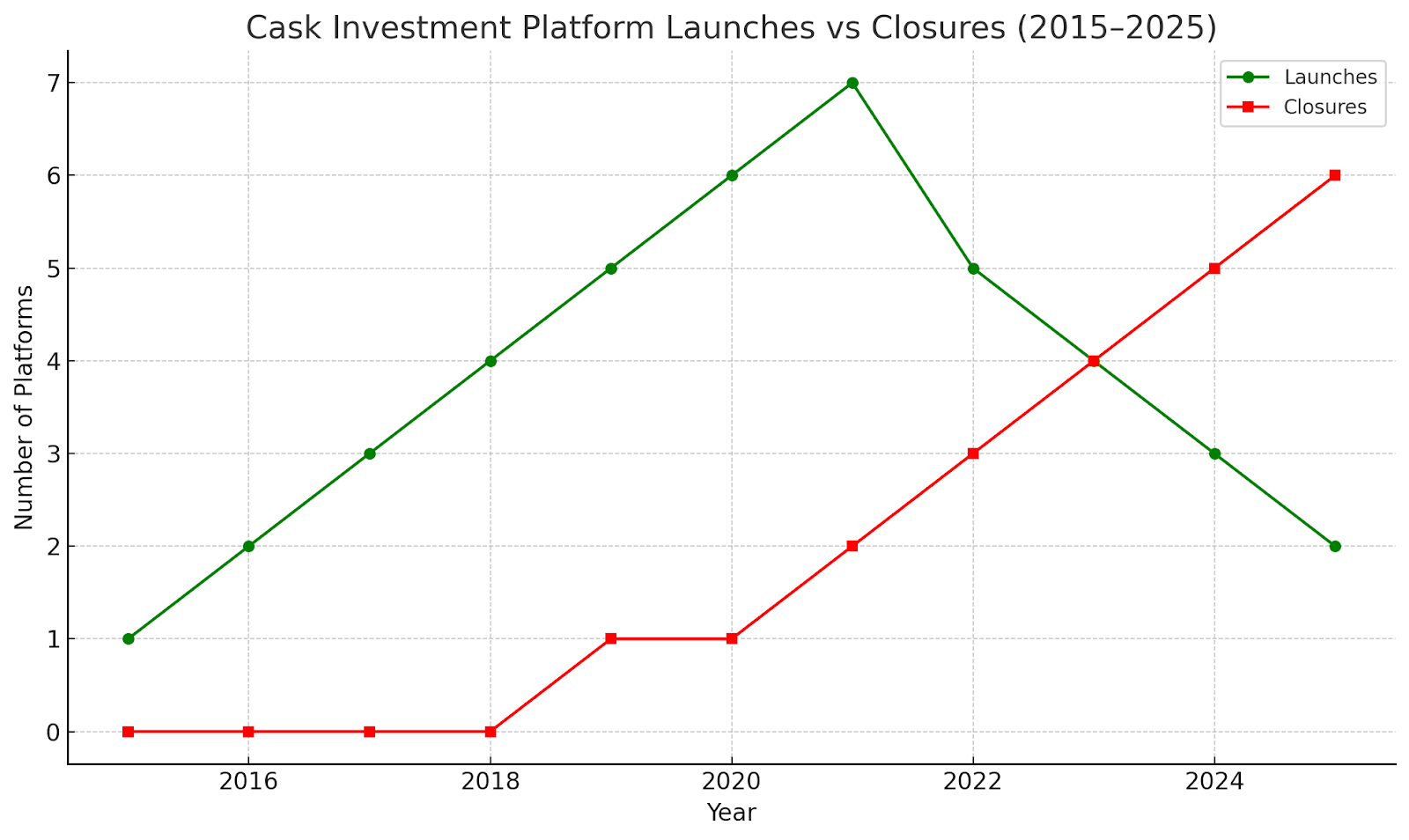

Barrels of trouble: The cask investment crash

Buying whiskey casks has been a seductive alternative investment play. But lately it has turned sour as multiple investment platforms have collapsed, in some cases leaving investors burned.

The pitch was seductive: low volatility, high returns, and a tangible asset. But the reality was messier: overvalued barrels, illiquid markets, nonexistent resale infrastructure, and custodial failures.

Case study: Whisky Merchants Trading Ltd.

In April 2025, Whisky Merchants Trading Ltd — the operator behind brands like Cask 88 and Braeburn Whisky — collapsed into administration.

This is the largest high-profile failure in the modern whiskey cask investing world. The company had touted managing approximately £80 million in whisky casks.

But when administrators took over, investors discovered they couldn’t actually locate their casks or verify ownership!

What went wrong?

The firm’s collapse exposed a big problem: investors held certificates, not warehouse-backed delivery orders.

For context, delivery orders are legal documents instructing warehouses to transfer ownership of casks to counterparties. These contracts are critical, because without them, legal ownership cannot be verified. In the case of Braeburn, many casks listed weren’t registered in investors’ names.

Investor fallout

Affected investors now face an uphill battle. Without delivery orders, most lack legal standing to claim casks — even if they have proof of purchase.

Investors are now in limbo. Warehouses can't confirm ownership, and administrators are swamped with claims.

Adding to the mess is that Braeburn Whisky and Cask 88 were linked through shell companies in Singapore and Spain, making follow-up difficult.

Teaghlach Holdings, the parent company, has been dissolved under UK law.

UK is cracking down

Whisky Merchants isn’t alone. Firms like Whisky Investment Partners and Cask Whisky Ltd have also drawn regulators’ attention for inflated pricing, impossible returns, and confusing corporate structures.

The UK’s Advertising Standards Authority has started cracking down on misleading marketing in the space, so enforcement is now catching up to the hype.

If you're an alternative investor and opened Instagram between 2017 - 2023, you likely saw a ton of ads for UK-based cask investment firms. But some of those glossy ads masked risky schemes, inflated prices, and vanishing accountability.

The lesson

Serious investors need to understand that without verifiable title, insured custody, and exit infrastructure, they’re not holding an asset — they’re essentially holding a promise. And in a volatile, lightly regulated space, promises can break.

Companies shouldn't be financializing whiskey without financial-grade infrastructure. Custodianship, insurance, regular valuations, and a credible exit path must be baked into any serious platform.

Those that build on shaky assumptions won’t survive. But done right, there’s still plenty of room for innovation and value.

Distressed French whiskey opportunity 🇫🇷

France’s whisky scene is new and booming. You may recall from a few weeks ago that we here at Alts were seriously considering buying a French whiskey distillery.

We identified a distressed distillery near Saint-Émilion called Maison Lineti and were considering acquiring it as a potential Altea deal.

Maison Lineti is located in the Bordeaux region — long famous for wine, but increasingly recognized for whiskey.

However, over the past few weeks, the deal has taken some turns. We're now looking to buy up the barrels and equipment only.

This has basically turned into an asset strip that gets us top-tier whisky for pennies on the dollar.

The whiskey industry is entering a new chapter — one defined less by hype and more by hard questions.

Do you have a truly unique offering? Can you command premium prices? Does inventory match demand? Have you earned trust? What's your track record? Can you prove that investors own the product?

For investors, owning the supply chain from top to bottom is always a smart play — albeit a capital intensive one. (This is exactly what Alts is doing with their stake in Herencia de Agaves Tequila Distillery.)

Asset-backed financing is another wise play. We've talked about wine trade finance, where merchants who need to buy inventory years before they can sell it open the door for smart, secured alternative lending. The same exact dynamic applies to the whiskey industry.

The next generation of financial products, stuff like tokenized whiskey through firms like Brickken, NAV-linked securitization, and centralized trading platforms, must learn from past mistakes.

Investors need to look for proof (hah) of purchase. QR codes, blockchain logs, and authentication tools are becoming table stakes for high-end whiskey. Brands that don't have transparency will likely find themselves pushed out of the premium tier.

Despite the setbacks, whiskey still holds promise as an alternative asset, and frankly this reset is a good thing.

It’s an opportunity for smarter production, more transparent investment platforms, and brands that align with what today’s consumer actually wants.

The ones that make it through this moment will be the ones that adapt clearly, quickly, and with conviction. 🥃

Morgan's responsibilities include drinking and knowing things. Before entering the world of alternative assets, Morgan worked in Americas Consulting at CBRE where he advised companies on their business and real estate strategies. He then pivoted to the investment industry, working as a Portfolio Analyst within Pagaya Investments, overseeing consumer credit, auto loan, and SFR strategies, before joining Apollo Global. Today, he is Chief Investment Officer at 1791 Capital Management and Private Portfolio Manager at BAXUS.

Disclosures

This issue was co-written by Morgan Roberts and Stefan von Imhof, with help from Finian Sedgwick. It was edited by Stefan.

This issue was sponsored by Gelt. No other company paid to be included in this issue.

Altea has holdings in Herencia de Agaves distillery