| Open the Flood Gates! Huge Surge in Overseas Students to Save the Inner-City Apartment Markets... |

Thursday, 26 May 2022 — Albert Park  | | By Catherine Cashmore | | Editor, The Daily Reckoning Australia |

|

[5 min read] Dear Reader, It used to be spruiked that immigration was the cause of high and rising property prices. But following two years of virtually zero immigration coupled with the biggest property boom since the late ‘80s — the blinkers are off. That’s not to say that immigration doesn’t add to the stew of all else being equal. Especially in Melbourne and Sydney, which have historically captured the greatest influx. It’s just that fat juicy homebuyer grants and government tax invectives, coupled with recent COVID migration trends, have had a far greater influence on the speed and direction of property prices than immigration per se. The incoming Albanese government, with their shared-equity scheme, know it. They won’t allow prices to drop on their watch. Still, one sector that has suffered significantly is the CBD apartment market. Particularly in Melbourne. There was always an oversupply — I used to quip that we’d run out of students before we ran out of inner-city high-rise apartments. Back in 2018, Melbourne City Councillor Nick Reece admitted as such. He said that many of Melbourne’s high-rise monstrosities were ‘crap’, poor quality construction: ‘“We have let too much crap be built,” Melbourne City Council’s planning chair Nick Reece says… ‘“We want to see more buildings that give back to the public realm,” says Cr Reece, who argues that while Melbourne is by far Australia’s most attractive and interesting city, it has been degraded by recent bad architecture and design… ‘“We are seeing low-quality design outcomes”…’

The sector was further decimated during the COVID lockdowns. Agents in the CBD and Docklands reported that that the market was ‘flooded’. There was an ‘unprecedented’ apartment apocalypse! Thousands of short-term rentals turned into long-term rentals. In truth, the only thing that could turn the trend was to ramp up immigration. It’s why, at the end of 2021, Nick Reece, now Deputy Lord Mayor of Melbourne, called for a ‘massive wave of new immigrants to help get the city back on track’: ‘Our city now needs a massive wave of new immigrants to help get the city back on track. ‘The population of Melbourne is projected to be 300,000 less by 2025 compared to where it would have been without the pandemic. While Australia will be almost one million people down. ‘Across Melbourne, businesses are facing acute labour shortages… ‘Australia had an immigration plan to help rebuild after World War II, now we need an immigration plan to help rebuild after the war on COVID… ‘To bring back the buzz in all its glory we need the Commonwealth to come to the party and open the borders to a welcome wave of new arrivals.’

Reece’s call has been heeded. The Australian Financial Review this week reported a huge surge in approvals for student visas from Nepal. Advertisement: The ‘Master Asset’ to Own in 2022 In 2021, the housing market rose at its fastest annual rate for 32 years. Both Sydney and Melbourne registered record-breaking double-digit growth. But two of Australia’s top financial forecasters recently went on camera to say that this is just the opening act of a $4 trillion superboom. Only this time, the uptrend will centre on a different property market. Watch here to find out where. |

|

The surge likely being driven ‘by non-genuine students who want to take advantage of the removal of a cap on the number of hours they could work and possible corruption of the visa approval process’. ‘There were 6312 applications from Nepal to study a vocational course in Australia, with visa approvals running at an exceptionally high 85 per cent. Application numbers for China and India, the two largest source countries for overseas students, were 3930 and 3483 respectively.’

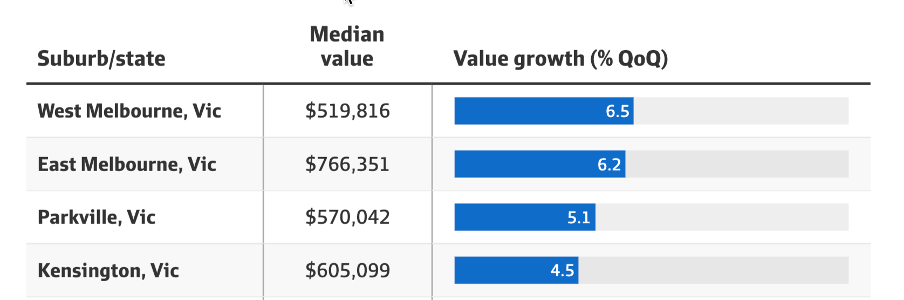

A turn in trend has been reportedly by CoreLogic. Some inner-city apartment markets rebounded strongly from the recent downturn: That’s not to say that apartments are now a great investment. The sector is riddled with risks for the unaware buyer. Poor quality construction, areas of oversupply, high owner’s corporation fees, and rising costs of insurance. But it does underpin why I advocate that it will take more to slow the market than small shifts in the cash rate/lending rate alone. Not forgetting to mention that Australia’s fourth largest lender, ANZ, has just cut its lowest variable rate back down to 2.29% for new customers! ‘“RateCity.com.au research director, Sally Tindall, said: “What these big bank cuts show is that competition in the mortgage market is still alive and kicking, despite the RBA hikes.”’

Onwards and upwards! Best wishes, Catherine Cashmore,

Editor, The Daily Reckoning Australia PS: Listen to my recent interview with Dr Cameron Murray as we uncover insights to Australia’s property market that challenge the mainstream narrative. | Cheated, Deleted, and Mistreated |

| | By Bill Bonner | | Editor, The Daily Reckoning Australia |

|

Dear Reader, What’s Paris like now? Poor Mr Macron — Chief of the French tribe — is one of the bright stars of the new rising generation of shameless technocrats. His administration was advertised as the standard-bearer for equality, justice, and net-negative carbon emissions. But now, two of his cabinet ministers have been accused of rape. ‘Sexual violence’ is the charge, which probably eases the burden of proof for the accuser. Meanwhile, COVID restrictions have been lifted. No more masks, no more ‘sanitary pass’, life is returning to normal in the French capital. Everything ever written about Paris is true. We don’t need to add to it. It’s a beautiful city, especially in May. The sun shines on the sidewalk cafes. Luxury brands gleam from the shop windows. And tourists are once again blocking our way on the sidewalks. A class apart Prices are rising, too. And the elite class — the leftish techno-snobs who run the country — are getting bolder. Their program: make life more and more miserable for the common man as they pursue their own jackass goals. ‘The citoyen will have to get used to living with less’, we quote no one in particular, ‘and following orders; so we can reduce our carbon output’. ‘It’s time for degrowth’, they add. ‘And if the costs fall disproportionately on the common man, well, too bad.’ The educated, enlightened, well-off Parisian believes the world would be a better place if the uneducated, unenlightened, struggling yokels were kept in their place. Specifically, he wants them to use less energy, stay at home, turn down the heat, and not make a fuss about rising prices. In France, as in the US, the deciders are a class apart. They have their agenda, hopes, schemes, and fantasies. And they don’t want ‘the people’ to get in the way. In the US last week came evidence that ‘the people’ are stumbling. The big retailers — Costco, Walmart, and Target — were hit hard. Earnings were disappointing, leading to the steepest stock market falls since Black Monday of 1987. On Friday, Target had its worst day in 35 years. Counting costs Adding to their costs is a big increase in fuel prices. These companies spend hundreds of millions on energy. As the energy price — especially diesel fuel — goes up, their margins are squeezed. And the available evidence shows the customer — the salt of the earth — is less and less able to afford to live in the manner he recently became accustomed to. The gimmie/stimmy is running out. Wages are supposed to be rising at a 5% rate. But consumer prices are rising even faster. Gasoline, for example, is up more than 30% in the last 12 months. Basic expenses — food, shelter, and fuel — are going up so fast that households have less and less left over for ‘discretionary’ spending, which leaves the big box retailers with a lot of unsold products in the box. And today, we feel their pain — the misery, desolation, and anguish of the working classes, both at home and abroad. These are the guys and gals with chainsaws and work belts…with 18 wheelers to edge into a tight spot…with a night shift to complete without falling asleep…with croissants to bake or laundry to wash. These are the people who made the world what it is. They fell on the Normandy beaches…built the Brooklyn Bridge…put down the hardtop roads…baked the cookies…and delivered the mail. And now, they are still the people who add the most real value to our lives. Not the hedge fund managers, influencers, or policymakers…but autoworkers, farmers, UPS drivers, cooks, baristas, waiters, carpenters, plumbers, and masons. And here’s the gist of our story: the masses have been cheated, deleted, and mistreated. And it’s going to get worse. In a nutshell, while the wealth of the crème de la crème was teased up by the feds, the working class — most of us — got nothing. The top 1% added US$36 trillion in wealth since 1999 — or about US$3 million per person. The bottom 50% added wealth too, but only about US$13,000 each. Each person at the tiny top got 230 times more money than those at the broad bottom. But all that froth came at a cost. The feds had no extra money, so they pushed down interest rates, borrowed, and printed money to cover the extra costs. The result was US$50 trillion worth of debt added to the US economy since 1999. Who will pay for it? We ‘the people’, of course. That is what the ‘inflation tax’ is all about. More to come… Regards, Bill Bonner,

For The Daily Reckoning Australia Advertisement: How to Invest in Tesla’s ‘Secret Supplier’ It’s a company most people have probably never heard of. And it just quietly cut a deal to supply Tesla with an often overlooked metal that’s critical to EV batteries (hint: it’s NOT lithium). That deal could cause the stock’s share price — currently less than $2 — to skyrocket. This isn’t widely known yet. But we have the full story here. |

|

|