| Does the Election Matter for the Market? |

Monday, 11 April 2022 — Albert Park  | | By Callum Newman | | Editor, The Daily Reckoning Australia |

|

[6 min read] - Scary headlines…but not reality

- Risks build in the commodity space

- Plus, does the election matter for the market?

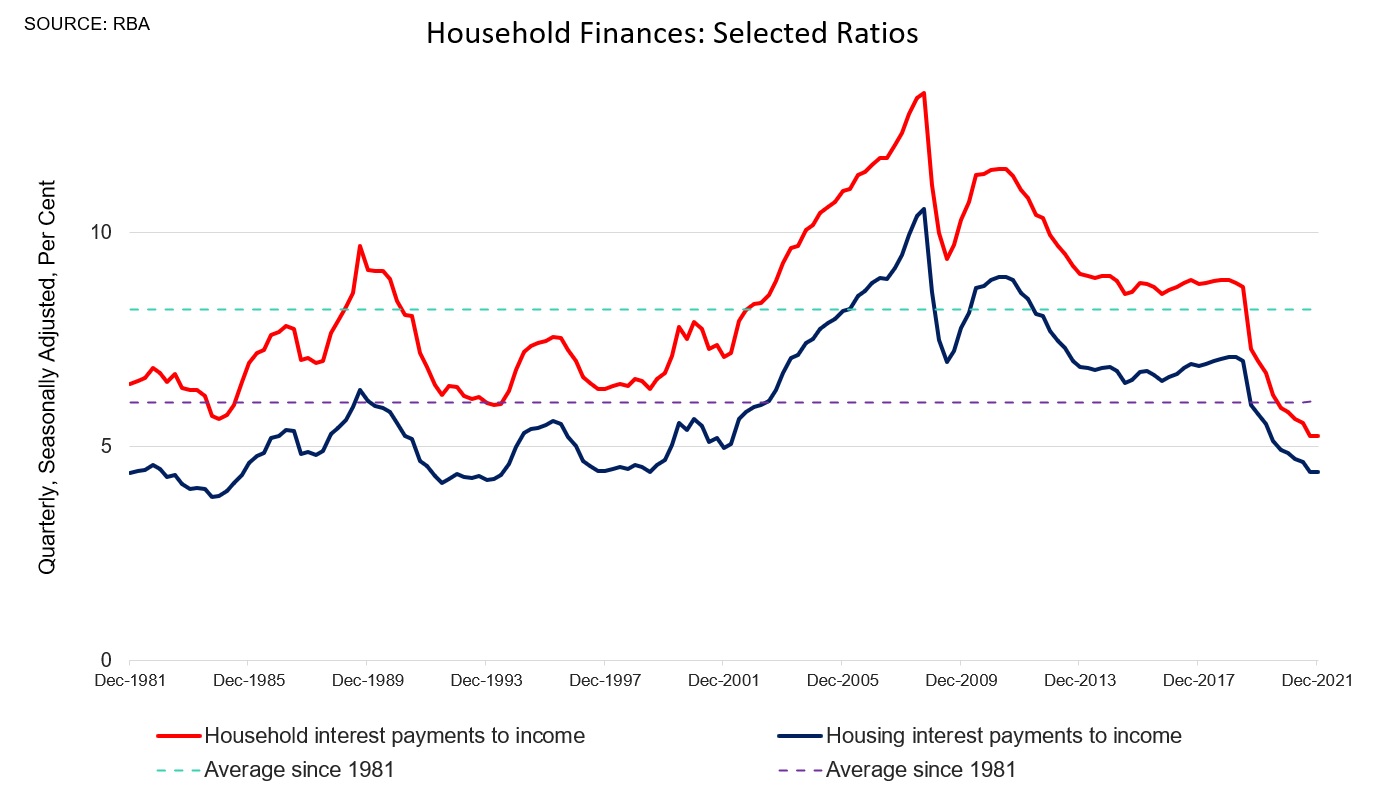

Dear Reader, 1) It helps not to be a lazy bum when it comes to investing. You sleep better. There’s no better example right now than the commentary around the release of the Reserve Bank’s ‘Financial Stability Review’. This is a document the central bank releases twice a year. It came out last week. The mainstream media latched on to a potential scenario where a 2% rise in mortgage rates could cut house prices 15%. Cue the scary headlines and fretting. I call that clickbait! What makes me say that? If you read the document, as I did this morning, it paints a very secure picture for the housing market. You get the complete opposite impression! Here’s some statistics that don’t make for juicy headlines. Data suggests: - Loans in negative equity are just 0.25%.

- Only 5% of loans have a loan-to-value ratio greater than 75%.

- Median buffer mortgage prepayments are 21 months for variable rate borrowers.

- 40% of loans are on fixed rates (double the number in 2020) at historically extremely low rates.

- Total credit growth continues to rise.

Oh, and household interest payments, as of now, are at a record low: None of the above looks very scary to me. Add in increasing immigration and low unemployment, plus big government deficits, and I’m not losing sleep about the housing market. Personally, I see lots of opportunity in the stock market around this. Property stocks have been hit in the last 12 months, on exactly these fears. That sets the stage for a rally if I’m right about these fears being overly discounted into stock prices. My next issue is going to contain three recommendations to take advantage of this. Stay tuned for more! Advertisement: The SMART way to play the rise of crypto With companies like Tesla, Apple, Microsoft, and Goldman Sachs adopting crypto — you might be thinking it’s time to make it part of YOUR long-term plans, too. And according to our top crypto experts, there’s a simple, smart move you can make today to do exactly that. It doesn’t involve speculating on any single crypto. For the full story — just click right here. |

|

2) There is always something nagging at the back of your mind when it comes to the financial markets. Right now, most of the commentary is around the Ukraine war, inflation, and the market pricing in a 2% rise in rates from the US central bank, the Fed. The current COVID calamity in China might be slipping by a little too much, to my mind, at least. What’s the story? China has a ‘zero-COVID’ policy. That means any outbreak results in staggering restrictions on huge numbers of people. Shanghai is the hot zone right now. That’s 25–26 million people! Some are said to be running low on food. I saw one suggestion that China’s food system is highly time-sensitive, with poor cold chain management. If ports and trucks can’t clear from either a) workers hit by the virus or b) the lockdowns, there could be panic and unrest as people go hungry or are worried enough to do something drastic about it. The Financial Times says COVID cases could hit 250,000 a day if the Omicron outbreak tracks Hong Kong’s events. Meanwhile, President Xi is trying to juice everything to ensure his third term is approved without a hitch later in the year. He’s latched his authority to this policy. Compounding this issue is that China’s vaccines don’t appear to be as effective as the Western ones, and millions of elderly Chinese aren’t vaccinated at all. Where this goes is anyone’s guess, but some blowback to Australia could be on the cards if Chinese weakness drags down commodity prices. With everybody trying to cash in on roaring lithium, iron ore, oil, and coal, there can’t be too many bears left in their caves. Or am I being too paranoid? Such is the madness the world of finance can take you to. How to cope with it? Let the market decide. There’s no need to act before. Until commodity stocks reverse powerfully in some way, we have to assume the market is comfortable with the risks presenting in China. But the situation bears careful watching. 3) ‘Does the election matter for the stock market, Cal?’ My brother asked me that yesterday. I don’t think so. It’s been said by others, but I think the following is true: there’s no economic difference between the two major parties. There was an opportunity when the Liberals won last time. That was a surprise…and it took up mortgage brokers, for example, that the royal commission previously toasted. The Liberals kept the same financial system (negative gearing, franking credits, commissions) in place. The market liked that…and so did voters, obviously. I don’t see an equivalent opportunity this time…just Australia’s ongoing political mediocrity. All the best, Callum Newman,

Editor, The Daily Reckoning Australia  | | By Bill Bonner | | Editor, The Daily Reckoning Australia |

|

Dear Reader, Whatever else can be said about it, this must be one of the most interesting and entertaining chapters in the history of central banking. Not since John Law slipped out of Paris in 1720, leaving in the dead of night to avoid an angry mob, has there been anything like it. Like Law, Jerome Powell has made a huge mess of things. A city slicker in the financial wilderness…with no compass to guide him, other than the Fed’s silly models and claptrap theories…he got hopelessly lost. And now he’s caught…trapped, between the inflation he created…and the reckoning he was desperate to avoid. Inflation has already returned to levels not seen since the 1970s. The Fed needs to stop printing; everybody says so. But if Powell fights inflation, the economy will collapse; it depends on ultra-low interest rates and free-flowing credit. If, on the other hand, he lets inflation rip, the dollar will die…bringing with it financial, social, and political chaos. Occasionally, a trapper or hiker will get stuck in the mountains, far from civilisation. He may break a leg…or like Aron Ralston in 2003…may get his arm pinned by a falling boulder. Ralston suffered for days. Then, near death, he had a vision of himself alive…but missing an arm. The next day, he took out his penknife and hacked off his arm, saving his life. Twice wrong In order to escape his trap, Jerome Powell needs to cut away 14 years’ worth of bad policy. Does he have the stomach for it? Could he endure the pain? We doubt it. But both from within the Fed and from the outside world, come hallucinations of successful surgery. Here’s JPMorgan Chief Jamie Dimon, in the Financial Times: ‘[Dimon] told investors he did not envy the Fed for the steps the US central bank would need to take to end its ultra-loose policies but urged it not to “worry about volatile markets unless they affect the actual economy”. “If the Fed gets it just right, we can have years of growth, and inflation will eventually start to recede. In any event, this process will cause lots of consternation and very volatile markets,” Dimon wrote.’

He’s wrong on both counts. After bumbling for so many years, there is no chance that the Fed will ‘get it just right’. Nor is it possible that genuine tightening wouldn’t ‘affect the actual economy’. Still, Powell’s compadres at the Fed press him to show a little courage. Here’s Bill Dudley, former inflation dove…now suddenly sporting sharp claws: ‘Investors should pay closer attention to what Powell has said: Financial conditions need to tighten. If this doesn’t happen on its own (which seems unlikely), the Fed will have to shock markets to achieve the desired response. This would mean hiking the federal funds rate considerably higher than currently anticipated. One way or another, to get inflation under control, the Fed will need to push bond yields higher and stock prices lower.’

And here’s another leading Fed voice, Lael Brainard, as reported by The Wall Street Journal: ‘“It is of paramount importance to get inflation down,” Ms. Brainard said Tuesday at a virtual conference hosted by the Federal Reserve Bank of Minneapolis. “Accordingly, the committee will continue tightening monetary policy methodically through a series of interest-rate increases and by starting to reduce the balance sheet at a rapid pace as soon as our May meeting.”’

As of Thursday afternoon, the Fed was bound and determined to do what needed to be done — and less! Here’s CNN: ‘The Federal Reserve is ready to raise interest rates at a faster pace to get a handle on America's pervasive inflation problem, according to minutes from the central bank's March meeting released Wednesday. ‘The minutes said “many participants” at the Fed's meeting in March noted they would have preferred a 50 basis point increase to the federal funds rate in light of high inflation.’

It almost makes us feel sorry for poor Jerome Powell. He clearly doesn’t know what he’s doing. He is, after all, a big city lawyer, lost in a Yellowstone of finance. No hope of rescue. No way out. And the catastrophe is underway…whether he acts or not. Piles of cash The COVID crisis caused the Fed to do a lot more of what it never should have been doing in the first place — printing money. In the last two years, its balance sheet (where the new money is tallied) rose more than it had in the entire 107 years since it was founded — by more than US$4 trillion. The money was then transmitted to Wall Street by buying bonds. But the Fed’s money printing ended last month. Now, as those bonds mature, the Fed’s balance sheet shrinks, and the US’s money supply shrivels. Quantitative Easing has given way to Quantitative Tightening, which is a whole different thing. And we’re not talking about small amounts. In 2020, the Fed added US$3 trillion of new money. Now, that money is scheduled to go away at the rate of nearly US$1 trillion per year. In other words, the Fed giveth — and unless it giveth more and more — what it gaveth will now go back whence it cometh. Along with it will go as much as US$50 trillion in fake, new wealth created since 2007…and a whole credit-addled economy, including trillion-dollar federal deficits, meme stocks, buyback programs, NFTs, zombie corporations, million-dollar shacks…and much, much more. The thought of it must trouble Jerome Powell’s sleep. But what can he do...puff up his courage…and try to remember where he packed his knife. Regards, Bill Bonner,

For The Daily Reckoning Australia |