| Another Day, Another Forecast of Falling Property Prices That You Should Ignore… |

Thursday, 10 March 2022 — Albert Park  | | By Catherine Cashmore | | Editor, The Daily Reckoning Australia |

|

[6 min read] Dear Reader, Another day, another forecast from one of the major banks throwing a dart to give their latest forecast for the housing market. This time, it comes from Australia’s biggest lender — the CBA: ‘The Commonwealth Bank is predicting overheated house prices will plunge in Sydney — and across Australia. ‘Median house prices in the Harbour City have spiked 23 per cent in the past year, but could drop nearly $200,000 by the end of 2023, analysis by the Commonwealth Bank shows. ‘The bank’s dwelling price projections predict the median house price across Australia will drop by eight per cent in 2023. ‘This includes a three per cent drop this year and a nine per cent fall next year in both Melbourne and Sydney.’

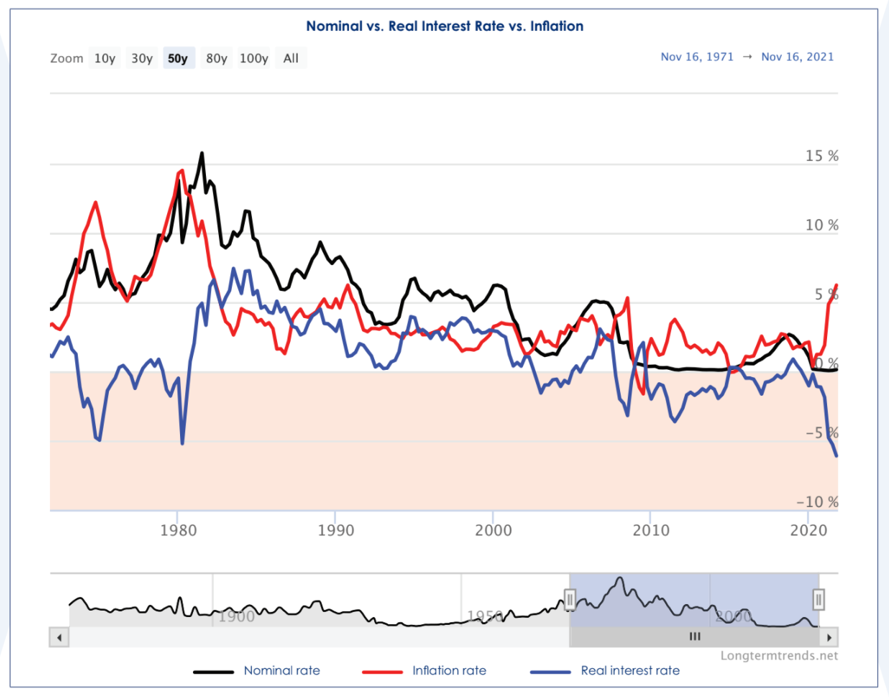

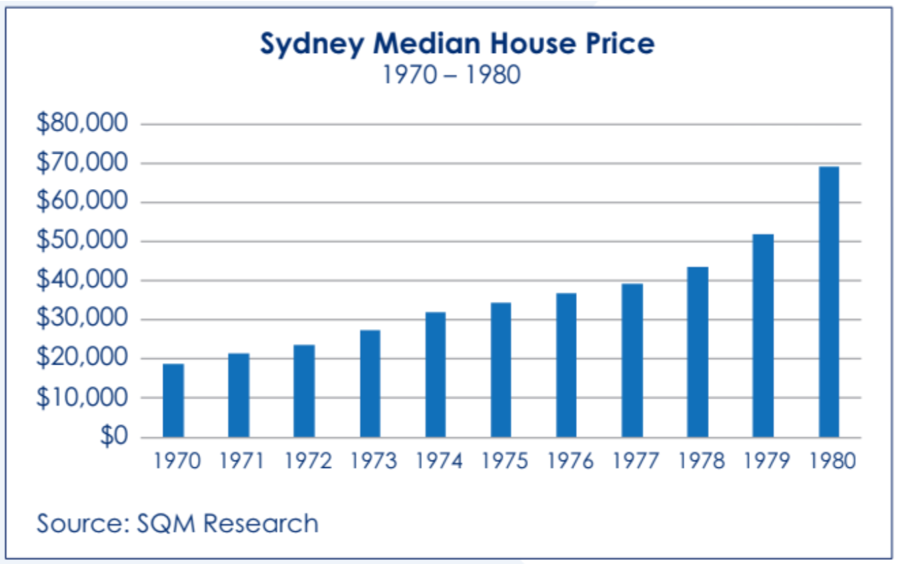

CBA doesn’t have a great track record. Their forecasts have been consistently wrong over the last few years — changing like the weather — along with the other major banks. Back in 2020, CBA warned that house prices would plummet by almost a third because of the coronavirus pandemic. Their worst-case scenario was a 32% drop by March 2023. By February 2021, with a rocketing boom underway in the Australian property market, CBA flipped. Their forecast changed to an increase of 16% over 2021 and 2022. It underestimated the boom significantly. Median prices were 25% higher by the end of 2021 and continue to climb, predominantly in the smaller capitals by population. Still, their latest forecast falls in line with the other majors. ANZ and Westpac are also predicting major falls in the property market in 2023. All of them have an appalling track record for accuracy. If they studied the land cycle — as we do over at Cycles, Trends & Forecasts — they would have advised their investors to scoop up property in early 2020, in preparation for the greatest real estate boom in Australia’s recorded history. This is precisely what we did, and those that followed our advice are now sitting pretty. Further, the forecasts are being made solely on the prospect of rising rates. There are a few things to consider when it comes to rising rates in an inflationary environment, however. Firstly, real interest rates (minus inflation) are negative — sitting at -2.9% here (and -5% in the US). If the RBA raised rates by 50bps (basis points), it may shock the market, but it still leaves real rates negative. Assuming inflation keeps pumping, as I expect it will, a small ramp-up in rates is not enough to produce a marked downturn. In other words, if housing prices are rising faster than a hike in lending rates, it could slow — but not stem — an upward trend. This is a point that Louis Christopher makes in his ‘Boom and Bust Report’. We can look back at what happened in the 1970s, when Australia’s inflation reached about 17.5%. Average lending rates were around 8–10%. Yet the median house price in Sydney tripled over the period: Granted, wage growth in the 1970s was rampant — far in excess of what we have today. But that’s not to say we’re not seeing strong wage growth in some sectors. The mining industry is a major one! New engineering graduates in WA are being offered salaries of $160,000 to work in the mines. Wages have increased by 27% in just 18 months! There aren’t enough workers for the jobs on offer. It’s one reason that over at Cycles, Trends & Forecasts we have had Perth as a top pick for investors. There’s also upward pressure on wages in other states. There’s an acute shortage of workers across many industries, including hospitality, construction, technology, medical, etc. In addition, companies have been forced to digitalise at a rapid pace. There’s no shortage of job opportunities, but there’s most certainly a shortage of talent. It’s yet to be seen if they will ramp up immigration to the levels needed to offset the trend. It won’t happen in a heartbeat. We’re still in a situation where more people are leaving Australia than arriving. Considering this, a small rise in interest rates (and therefore lending rates) would follow improvements in the economy (wage growth, etc.), and rises in median property prices would follow. The important point here is that land prices rise with inflation. More so due to the current drivers of inflation: - Shortages in commodities and manipulated disruptions to the supply chain. This is impacting construction. Projects are being delayed and new property values are being ramped up to cover construction costs.

- Massive stimulus spending outside of any prudent economic analysis catapulting us toward CBDCs (central bank digital currencies).

This is just one reason why we’ve had the fastest period of growth since 1989. We can expect Melbourne and Sydney to pull up early. I warned late last year in The DR that this would occur. Migration is flowing away from both states. However, this is not the case in other areas of Australia. If you give the above reports of major price falls in 2023 any energy, you’ll be making a big mistake. The peak of this current market cycle won’t occur until 2026. Find out why by clicking here. Sincerely, Catherine Cashmore,

Editor, The Daily Reckoning Australia  | | By Bill Bonner | | Editor, The Daily Reckoning Australia |

|

Dear Reader, ‘Nowhere else does an economy work like this.’

A friend in Buenos Aires Argentines have been living with inflation for a long time. It was 2,000% in 1990. It’s 50% now. If they don’t know how to survive it, no one does. Can we learn from them? We might have to. Here’s Business Insider: ‘US stocks fell on Monday, with the Dow Jones Industrial Average down 800 points and the Nasdaq ending lower by over 3% as investors weighed the impact of surging oil prices and eyed possible new sanctions on Russia's energy sector. ‘The geopolitical turmoil has sent commodities reeling, as wheat, nickel, gold, and oil all soared during Monday trading.’

A nearby news item shows regular gasoline at US$6.95 a gallon. And the price of oil itself rose to US$139 a barrel. Both experience and ‘the experts’ say a recession is stalking us. Meanwhile, Congress is working on a bill to exclude Russian oil from the US market. Thus, the US is attacking the three key elements of modern prosperity all at once — energy, money, and trust. It cuts off supplies of oil, it undermines the dollar with sanctions on honest savers and investors, and inflation and sanctions erode trust in the whole US-dominated financial system. Where this leads is anybody’s guess. But somewhere, faintly in the distance, we hear a tango beat. El Fin del Mundo Our man in Buenos Aires continued: ‘You look around, you see people living fairly normally. You see people with new cars — although there aren’t many of them. You see houses being built. You see people out and about, having a nice dinner or shopping. ‘If you had 50% inflation in the US, it would be another story. It would be a hellacious disaster. You’d have a revolution. (Our contact used to live in Miami.) People depend on credit. They have mortgages to refinance. They have debts to pay. The system depends on credit. Everything is sold on credit. If interest rates go up, the whole economy collapses. ‘That doesn’t happen here, basically because the economy already collapsed long ago. People don’t have mortgages. They don’t have debt. Nobody cares about interest rates because they can’t borrow money anyway. ‘As soon as people get money, they spend it.’

Seems simple enough. When you have money, don’t try to save it. But what do you spend it on? Our friend went on: ‘Real estate. Prices are low here. People buy now…and then they wait for them to go up again. That’s another part of the formula. Here, we go in Biblical cycles. Seven good years. Then, seven bad years. Sometimes we are the cheapest country in the world; then we’re the most expensive. Right now, we’re in bad years. So people take their money and add on to their houses…or buy an apartment. The rents are low too, so yields are poor. But prices will probably go up in the 7 good years. ‘And by the way, there’s a political cycle too. The Peronists (nationalist, socialist, populist) are in power now. But they’ve made such a mess of things, voters will probably turn away from them in the next election, in November. Then, we’ll see some good times, before the bad times come back.’

Buenos Aires is a treat. Lively. Sophisticated. Cheap. The food is good. The weather this time of year is delightful. The cafes and restaurants are busy. People seem to live well. But there’s more to the story. Here, the economy only works because people have learned to cheat. Money caves Our friend continued: ‘The nice thing about living here is that the government does the dumbest things. But they are intentionally incompetent. The rules and regulations are never well enforced. There are always ways around them. Take a look over there…’

He motioned to a place across the street: ‘There’s a “Cueva” [a black-market money exchange…literally, a “cave”]. It’s illegal. But the government knows it is there…and they’ve put a policeman out front so you know it’s safe to go in there. ‘We’re supposed to be having an economic crisis here. But I have a hard time hiring good workers because they can earn more by working remotely for a European or American company. Then, they get most of their pay transferred in cryptos… which is converted to pesos by these cuevas. No trace. No taxes.’

Were it not for the black market, Argentina would be an even bigger mess than it is now. The cuevas are tolerated because they attract foreign currencies…and the country needs foreign currencies to pay its foreign debts. The result is that there are people with money to spend. Of course, in the poor neighbourhoods it’s another story. There, people are trapped. They have no bank accounts in Miami. Nor do they receive cryptos via the internet. Their incomes, sometimes pitifully small, come from normal jobs and are paid in pesos. Government handouts too are in pesos — and lose value rapidly. Our friend concluded: ‘It really creates two separate economies. One of them is miserable and desperate. The other enjoys a very high standard of living. ‘But I don’t think the US is ready for this kind of thing…Americans still trust the government. They don’t know how to duck and dodge. And the government would never tolerate a black market like this.’

Regards, Bill Bonner,

For The Daily Reckoning Australia Advertisement: ASX’s first ‘industrial metaverse’ stock ripe for takeover (currently trading at 50 cents) Early big bets on the metaverse megatrend — Meta and Roblox — are getting turned on by investors. Here in Australia, though…on the other side of the planet to Wall Street and Silicon Valley… …the first chapter in a DIFFERENT kind of metaverse story is about to be written. And…if we’re right on one 50-cent ASX company…it could be about to have a giant takeover target put on its head. On 17 February, we made this an urgent buy recommendation for early speculators. Find out why here. |

|

|